IN TODAY'S ISSUE:

- Bitcoin had a stellar quarter, up 71.9%, and outperformed every other asset class

- The ongoing banking crisis thrust bitcoin into the limelight and given its technical and economic features gave the asset and technology the opportunity to shine

- Bitcoin’s performance comes despite heightened scrutiny from regulators for the broader crypto landscape, as well as law enforcement officials

- We continue to watch three important legal cases which may shape the face of the digital asset landscape going forward

- Bitcoin’s correlations with assets such as equities continued to fall, strengthening the diversification benefits of bitcoin ownership

- Hash rate zoomed to a new high as miners energize new rigs and economics remain favorable for miners with low electricity costs

- We continue to watch signs of stress on the banking system but suggest looking at credit creation avenues provided by the Fed, rather than just a narrow subset

- Bitcoin’s cycle price action around halvings appears to still be at play, with the drawdown continuing to look like the prior two

Performance Review

Bitcoin's Bang up Quarter

The price of bitcoin skyrocketed during the quarter rising 71.9%, far surpassing all other asset classes. This meteoric rise comes even as US regulators sought to clamp down on activity across the space, bringing enforcement actions and the threat of more enforcement action against many players in the industry. A couple of factors were at play that contributed to bitcoin’s performance. First and foremost was the banking crisis that continues to embroil regional banks in the US. While bitcoin’s usefulness in risk-off market scenarios and inflationary environments continues to be hotly debated, without a doubt bitcoin shined when it was needed most when faith in the very banking system was in question. It wasn’t just bitcoin that had a great quarter though, stocks, bonds, gold, and commodities were all up--although none close to bitcoin. We think this is owed to a more favorable macroeconomic backdrop, with declining (although still not tamed) inflation, and declining interest rate expectations. The headwind of 2022 has reversed course and is now acting as a tailwind. The final factor we think was at play was the cyclical nature of bitcoin prices. Bitcoin's reward halving is a little over a year away. This part of the cycle, following a precipitous drop like that one experienced in 2022, is usually the start of another cyclical upturn.

First Quarter Performance a Harbinger of Things to Come?

This was bitcoin’s fourth-best first quarter ever. An analysis of previous first quarters indicates they have been good omens for the rest of the year. Bitcoin has never had a down year after a positive first quarter and some of its best first quarters, like in 2011 and 2013, led to massive full-year returns. Given bitcoin’s maturity, those types of returns are unlikely to be achieved again, but the more important point is that strong first quarters have preceded even better returns. On every metric, the second quarter has been even better historically than the first quarter (win rate is the percentage of positive performances). While we won’t make predictions about the future, we are excited about things to come.

Correlations With Equities Decline, Rise with Gold and the Dollar

Bitcoin’s correlations with “risk-on” assets, like US equities, have been steadily declining this quarter. Correlations peaked in mid-2022 amidst an investment environment dominated by macroeconomic conditions and monetary policy decisions. Those factors, while still important, appear to be on the decline today, letting the idiosyncrasies of the asset and technology, such as network adoption, usage, and transaction volume, take over. Bitcoin’s correlations with gold ticked up in the last few weeks as the banking crisis demonstrated the need for stores of value outside of the traditional financial system. Regarding the US dollar, bitcoin’s correlations remain negative but rose during the quarter.

Over the long term, bitcoin’s average correlations with other asset classes remain extremely low. Bitcoin’s heightened correlations have been a new trend borne out of the fiscal and monetary stimulus impulses in response to the Covid-19 health care crisis. Given bitcoin’s growing adoption into traditional portfolios, it makes sense that the near-zero correlations exhibited prior to 2020 would increase, but still remain low given that the asset continues to be driven largely by idiosyncratic factors.

The Events that Shaped the Quarter

NFTs Come to Bitcoin

In January, Ordinals, a project that allows users to create non-fungible tokens (NFTs) natively on Bitcoin’s blockchain, launched. Its popularity sparked the imagination in the technical community and reignited an important philosophical discussion on how its blockchain should be used. While the growth of Ordinals inscriptions (NFTs) has slowed a bit since the initial craze, the number of inscriptions has topped one million to date, and one of the premier NFT creators in the entire digital asset landscape, Yuga Labs (Bored Apes Yacht Club, Crypto Punks), launched a collection, Twelvefold, using Ordinals. The philosophical debate on how Bitcoin’s blockchain should be used is one that has a long history, with no clear resolution. Financial purists continue to advocate for the use of Bitcoin for the transmission and storage of value. In contrast, those with more expansive views advocate for Bitcoin’s use as a data storage layer.

Regardless of which camp one falls into, the net beneficiary of the growth in inscriptions has been miners, who are paid transaction fees based on the amount of data transmitted. Bitcoin transactions are denominated in sats/vbyte (satoshis per virtual byte). Because inscriptions take up a lot of space, in one case nearly the entire 4 MB block size, the increased data transmission and storage has caused transaction fees paid to miners to rise.

Banking Crisis a Boon for Bitcoin

Fireworks erupted in the traditional banking sector with the takeover, wind down, or emergency sale of several banks. At the center of the crisis has been a liquidity issue, losses on the asset side sustained in a rising rate environment, and a skittish and concentrated deposit base. This resulted in an old-fashioned “bank run” although in a digital age, a bank run in a fractional reserve banking model can transform a liquidity issue into a solvency issue. The sudden loss in confidence in Silicon Valley Bank (SVB) for example resulted in depositors yanking $42B, or 25% of its deposit base, in a single day. Reportedly, the day SVB was closed by the FDIC, depositors had requested to withdraw over $100B of deposits, which would have nearly wiped out SVB’s deposit base.

Amidst this crisis in confidence, which also claimed Signature Bank and Silvergate, both crypto-friendly banks, bitcoin performed admirably. The price reaction of bitcoin during the quarter speaks volumes about how investors think about bitcoin during a banking crisis. The jury may still be out on its applicability in inflationary environments or as a financial market risk hedge, but bitcoin aced the test on how it reacts when confidence in the financial plumbing is questioned. Bitcoin’s continued operation when the financial institutions of the world sustain failures might be one of its best attributes.

Banking Constriction Engulfs Digital Asset Service Providers

The first quarter banking crisis resulted in the wind-down and receivership of two important cornerstones of the digital asset ecosystem, Silvergate Bank and Signature Bank, respectively. Both banks had real-time settlement networks that were heavily utilized by trading firms and other digital asset service providers to efficiently move funds 24/7. The loss of these crypto-friendly banks and the well-publicized loss of banking relationships by several other digital asset service providers sparked industry fears of a coordinated attack by banking regulators on crypto. While no evidence supporting the idea has surfaced, concerns have not abated across the industry. It may just be that banks have heightened client concerns given the realizations of the industry practices in 2022 or that digital asset clients might represent deposit base concentration and a flight risk. We do know that some banks remain friendly to crypto companies and that the failures of Silvergate and Signature represent opportunities, rather than risks, for some banks.

Regulation Front and Center

To say that regulators and law enforcement were active across the digital asset landscape during the first quarter is an understatement. Two quarters ago we were hopeful that 2023 would bring legislative clarity to the industry, but instead of clarity brought by new legislation, today the industry is dealing with the fallout from the calamitous events of 2022. We still may ultimately see legislative clarity and with it new rules for regulators, but until that time we will be in an environment where regulators use existing authority. While many of these cases are important, we think the ongoing Ripple litigation with the SEC, the Wahi insider trading case with the SEC, and the Grayscale case against the SEC are the most important ones to watch now. All these cases are now in the hands of federal judges, and some may ultimately end up before the US Supreme Court. While these three cases are what we think are the most important, the following is a summary of regulatory activities during the quarter related to the digital asset ecosystem.

Banking Regulators

- Fed, OCC, and FDIC release joint statement on the risks digital asset pose to the banking system

- Fed policy statement says that holding crypto assets in principal or issuing digital assets, including stablecoins, is unlikely to be consistent with safe banking practices

- Fed denies Custodia Bank’s application to the Federal Reserve System

NYDFS halts the creation of the BUSD stablecoin issued by Paxos - NYDFS announces $100M settlement with Coinbase over its compliance program

- NYDFS updates bankruptcy protection guidance for crypto custodians

Securities Regulators

- SEC charges Gemini and Genesis for lending products

- SEC obtains $45M settlement from Nexo in connection with its lending products

- Kraken pays $30M to settle SEC charges associated with its staking services

- SEC charges Beaxy exchange for the operations of an unregistered exchange, broker, and clearing agency

- SEC charges Justin Sun, settles with 8 celebrities for non-disclosure of endorsements

- SEC proposes updated rules, including digital assets, for qualified custodians that service RIAs

- Coinbase receives Wells notice from the SEC, potentially implicating many of its business lines

- Paxos receives Wells notice related to its BUSD stablecoin

- SEC brings charges against Terraform Labs CEO (LUNA/UST assets) Do Kwon

- NYAG charges KuCoin for failing to register as a securities and commodities broker dealer

- Judges hear oral arguments in Grayscale’s lawsuit against the SEC

Commodities Regulators

- CFTC charges Binance and its CEO Changpeng Zhao with willful evasion of federal laws and the illegal operation of a derivatives exchange

Criminal Enforcement

- DOJ brings charges against Bitzlato executive for unlicensed money transmission

- DOJ brings charges against Terraform Labs CEO (LUNA/UST assets) Do Kwon

US Treasury

- FinCEN identifies Bitzlato exchange as a primary money laundering concern

Treasury releases report on illicit finance risk in DeFi

Executive Branch

- White House announces roadmap to mitigate risks in cryptocurrencies

- Economic Report of the President is critical of cryptocurrencies

Network Hash Rate Zooms to a New High

The Bitcoin network’s hash rate, a proxy for the computational effort brought to bear by miners, hit a new all-time high this quarter. Economics remain favorable to miners, with marginal production costs (electricity) for the lowest-cost miners in the $7-$8K range. Given those economics, miners that have been able to secure power capacity have been energizing their miners, growing the network hash rate.

With the hash rate hitting a new high but the price also rallying the network hash price, the value of a miner’s hash, has lifted off the late 2022 lows. Hash prices are still well below the 2021 highs, but that does not mean miners cannot generate profitability given where breakeven prices are today.

Fund Flows Muted Once Again

Despite the large price rally during the quarter, exchange-listed funds around the world showed a net outflow of $34M for the quarter. This is the third consecutive quarter with little net change in either direction. The last big inflow was around the ProShares Bitcoin Strategy ETF launch in 4Q21.

Looking Ahead

Fed Balance Sheet Jumps as Banking Crisis Take Hold

With the regional banking crisis unfolding throughout the quarter, supportive measures employed by the Fed resulted in a jump in the size of its balance sheet. For the past year, the Fed has been engaged in both raising interest rates and a reduction in its balance sheet (quantitative tightening) by allowing the securities it owns to mature without repurchasing more (runoff).

The Fed continues to allow its securities portfolio to run off, but the emergency measures that were required during the quarter, such as the creation of new lending facilities (Bank Term Funding Program) and access to the discount window, resulted in credit extension and therefore the growth of the Fed’s overall balance sheet. Examining any one credit extension mechanism might be misleading, especially in comparison to past crises so we created the following chart, which measures all credit extended by the Fed (total factors supplying reserves minus total securities held). While these measures have jumped significantly, they are still well below the levels of the Global Financial Crisis and COVID-19.

An important trend to watch in the coming quarter is how this credit extension evolves with the ongoing banking crisis. Investors remain on edge regarding bank balance sheets with concerns about unrealized losses caused by rising interest rates now morphing into credit fears. The Fed has a number of tricks up its sleeve it can pull if the crisis continues, such as lowering interest rates and quantitative easing, but the draw on these credit facilities is the first thing we would watch.

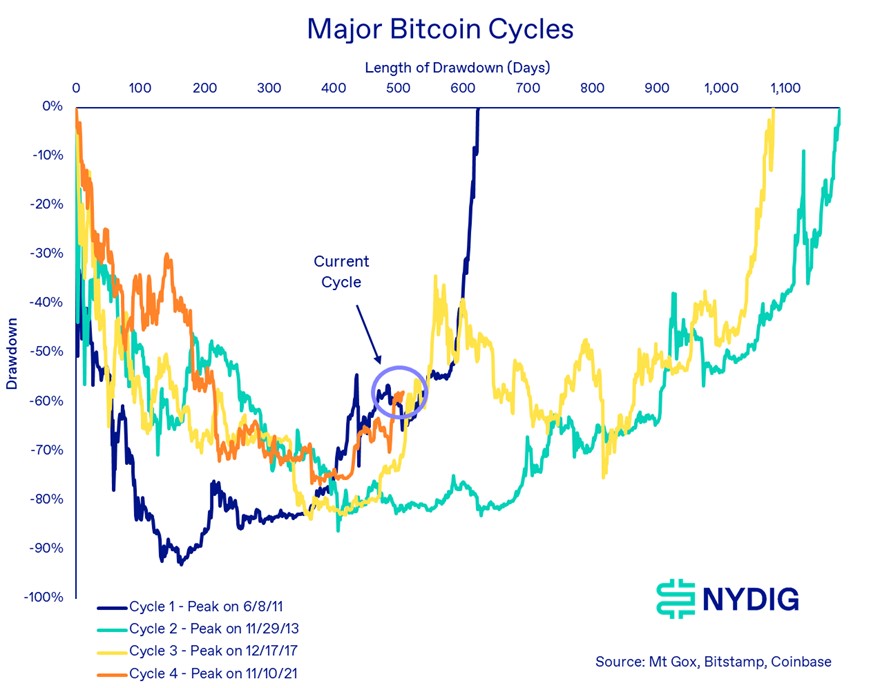

Digging Out of the Drawdown

As of the end of the quarter, it was 506 days since bitcoin’s cyclical price peak in November 2021. Despite all the unique events that have unfolded in the past during the current drawdown, this cycle looks similar in depth and duration to previous cycles. If bitcoin were to follow the previous 2 cycles (the first cycles were markedly shorter), bitcoin would recover to its prior peak of $69K sometime at the end of 2024. The industry is confronting factors, however, such as increased regulatory scrutiny that may make things look slightly different.

Having Cycles Still at Play

In May 2024, Bitcoin will undergo its fourth block subsidy halving, the foundation of Bitcoin’s scarcity function that caps supply at 21M bitcoins. The upcoming halving will take the reward paid to miners from 6.25 bitcoins to 3.125 bitcoins per block. In the past, bitcoin halving events have been important markers in its cycle price pattern, marking roughly halfway between two cycle highs. We are keeping an eye out to see if these patterns hold, with the same caveat regarding drawdowns, that historical returns might not be indicative of future performance.

Concluding Remarks

It was big quarter for bitcoin, and while we like to point to price performance as the most important indicator, the reality is that it is simply the byproduct of the asset's importance during a banking crisis. A decentralized, permissionless, and censorship resistant store of value outside of the traditional banking system sounds like an unnecessary luxury during most times, but it becomes essential during times we just experienced. It has been nearly 15 years since the world experienced a major banking crisis, and while we cannot predict the duration or severity of the current banking woes, this time investors have a new option in their investment arsenal. Price cycles appear to be following a familiar pattern, and while regulatory activity is unlikely to die down, this performance comes despite heightened industry scrutiny. For those reasons, bitcoin's dominance, its share of the industry market cap, has been on the rise, and there are reasons to think that might continue to hold.