IN TODAY'S ISSUE:

- Bitcoin rose a whopping 57.4% during the seasonally strong fourth quarter, as the long-awaited spot ETF gets closer to launch. On the year, bitcoin was up 156.9%, far surpassing all other asset classes.

- We expect numerous spot ETFs to be approved by the SEC by next Wednesday, January 10th, and we find calls to the contrary neither credible nor compelling.

- An ETF could begin trading shortly after the exchanges’ listing applications are approved given the SEC has met with the various ETF issuers and exchanges 28 times since mid-November.

- Expectations are clearly running high into the event, however, with Bitcoin adding $339B in market cap since the filing of the iShares S-1 touched off this race.

- The launch of spot ETF could have meaningful impacts on other financial instruments, such as futures and the BITO ETF, potentially permanently altering market features such as the “futures basis.”

- Historical price cycles continue to be largely repeated, albeit with this recovery tracking ahead of the prior two drawdowns both in terms of duration and severity

- After the ETF news is digested, all eyes will turn to the halving in mid-April, an important marker for price cycles, but not the material supply overhang reduction ($18M/d) that some believe given the multibillion dollar daily spot markets.

- BRC-20s and Ordinals have become a material driver of miner revenue (network security) via transaction fees, lessening the impact the halving would have had on miner economics prior to their invention.

Performance Review

Bitcoin Zooms Up, Ends the Year on a High Note

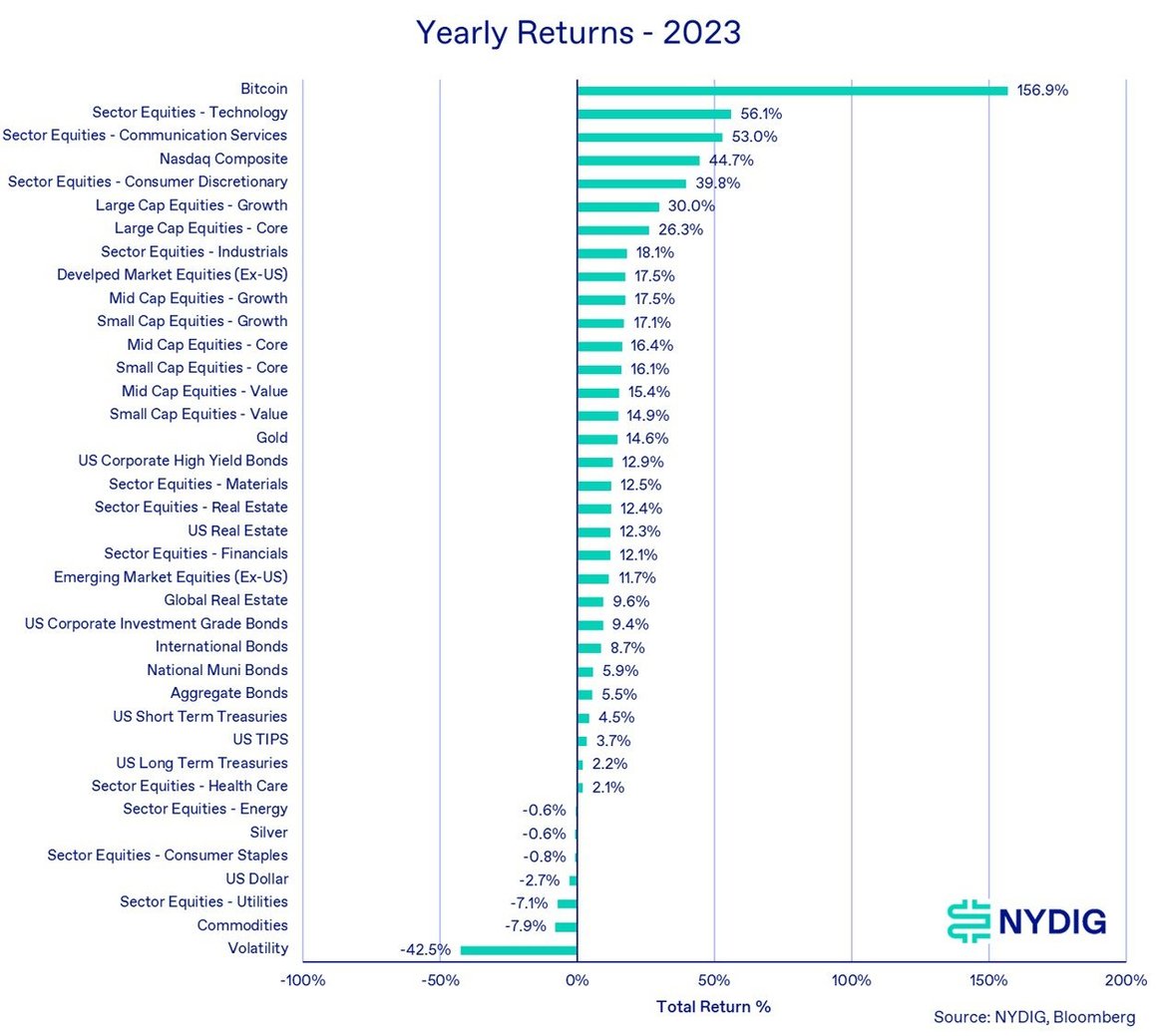

The price of bitcoin rallied a whopping 57.4% during the quarter, bringing its year-to-date return to 156.9%. Quarterly returns were driven by continued optimism for the approval of a spot bitcoin ETF, which is expected in early January. The fourth quarter is usually one of bitcoin’s strongest from a price performance perspective, and while the 57.4% is impressive, it was only bitcoin’s 6th best fourth quarter ever, highlighting how powerful this period has been historically.

Most other asset classes performed well during the quarter as waning inflation data provided the backdrop for declining forward interest rate expectations. Stocks, bonds, and precious metals rallied, while the US dollar and commodities fell. The gold rally (precious metals) was driven by declining real interest rates, which peaked in October using the yield on 10-year TIPS, rather than rising inflation. The fall in the US dollar (compared to other fiat currencies) likely also had to do with declining real interest rates, while commodities were driven largely by oil prices and excess supply.

Bitcoin’s 156.9% return for 2023 far outpaced equity markets, even tech and communications equities, which had a banner year. Most asset classes were up on the year, with the exception of defensive equities (staples and utilities), commodities and energy linked equities, the US dollar, and volatility measures (VIX). As with the fourth quarter returns, the 156.9% return marked bitcoin’s 6th best year.

4Q Seasonality Delivered

The fourth quarter historically has been one of bitcoin’s strongest from a price-performance perspective and this year kept with that trend. Bitcoin’s fourth-quarter performance is also highly correlated with the annual return, with a correlation ratio of 88%. Given that bitcoin was already up significantly through 3Q, given that correlation statistic, one might have been able to surmise that 4Q would have been a good quarter ahead of time.

Correlations Revert to Long-Term Averages

Bitcoin’s correlations with other major asset classes, particularly equities, have fallen from their post-Covid stimulus peaks and reverted to their long-term averages of about zero. That’s positive news for investors as bitcoin’s correlations (or lack thereof) have the ability to reduce risks in multi asset portfolios. It is clear to us that the pushing and then pulling of liquidity in financial markets via monetary (interest rates) and fiscal (government spending) that have occurred in the past 3 years, first in response to Covid and then as a reaction to the inflation, materially impacted asset class correlations. Through much of 2022 and 2023, even stocks and bonds were highly correlated, antithetical to the underpinnings of the 60/40 portfolio.

The Events That Shaped the Quarter

All About ETFs

Without a doubt, the machinations surrounding the approval of a spot bitcoin ETF were the most important events this quarter. While it may not be evident from the previous chart, every undulation, every twist and turn in the process was pored over by the market. It started with SEC failing to appeal the DC Court of Appeals ruling in the Grayscale case, which stated that SEC acted in an arbitrary and capricious manner in denying its effort to convert the Grayscale Bitcoin Trust into an ETF. With the SEC failing to appeal the ruling, it set the stage for the SEC to either come up with new grounds to deny spot ETFs, one different from the reasons it had been using for several years, or to gear up for their approval. After numerous meetings with fund issuers and updated registration statements, today the final decision is on proverbial “one yard line," and we expect the SEC finally approve many of the spot ETFs in contention.

Of course, approval is not guaranteed. The SEC can absolutely come up with new grounds for disapproval, but it cannot rely on its previous reasoning. The SEC has also met with issuers 28 times since late November, to get issuers in-line with its desires, particularly on the “cash” create/redeem methodology vs “in-kind,” which has been favored by issuers. But at this point, every major issuer has either removed the “in-kind” methodology entirely from their registration statements or are awaiting upon regulatory approval for "in-kind" creations and redemptions, whenever that may be. SEC meetings with issuers have generally gone from the Division of Trading and Markets (approves exchanges’ 19b-4 filings), to the Office of the Chairman, to the Division of Corporation Finance (approves registration statements). For the SEC to do an about face and deny these applications after so many meetings is certainly within its wherewithal, but it would be out of character, in our opinion. We reject a recently published report that the SEC would deny the applications on the grounds that the assertions put forth in the report are based on illogical premises, poorly constructed arguments, a meager understanding of the regulatory process. As a reminder, some ETFs are currently in the public comment period, which ends on January 5th. Given the final response deadline of January 10th for the ARK 21Shares application, we (still) think that a final decision comes January 8th - 10th.

FASB Issues Guidance on Accounting for Crypto Assets

In mid-December, after many months of working on the matter, the Financial Accounting Standards Board (FASB) issued guidance on the accounting for digital assets, including bitcoin. Prior to the guidance, there had been no explicit standard, so most companies treated it as an intangible asset, marked at cost, periodically tested for impairment, and written down in the event of a price decline but never written up. Now we have a regime, which when it goes into place a year from now, will mark bitcoin at fair market value, marking it both up and down in price. This more accurately reflects the economic substance of bitcoin and removes a hurdle for investment purposes.

Ordinals/BRC-20s Have a Resurgence as Fees Ramp to All Time Highs

Bitcoin’s transaction fees, the tips senders use to entice miners to stamp their transactions into blocks, soared to an all-time daily high this quarter. Most of this was driven by BRC-20 transactions, fungible memecoins issued using the Ordinals protocol. BRC-20s as a category have reached $1.8B in aggregate value creating substantial trading volume, movement on the blockchain and the issuance of new coins.

Transaction fees, even in BTC terms, tend to be positively correlated with bitcoin price, peaking daily at or near cycle price highs, which is why this recent ramp in fees is so interesting. It is unlikely we are near a price cycle high (midcycle inflection point, maybe), so what we are seeing is genuine usage of Bitcoin blockchain, even if it is for speculative purposes on BRC-20s. It is unclear whether “memecoin season” will continue, but it is clear to us that if you give speculators a way to make money, they will use a blockchain or technology.

Hash Rate Climbs 115% in 2023

Bitcoin’s hash rate, the measure of the rate at which the aggregate mining ecosystem is randomly searching for solutions to new blocks, zoomed to new all-time highs this year. To see the network hash rate recently break 500 EH/s is a remarkable turn of events from a year ago when the price of bitcoin was in the doldrums and many miners were financially stressed, with bankruptcy claiming Core Scientific and Compute North. Throughout 2023, the network added +23 EH/s per month of hash power. The hash rate at the beginning of the year was only 241 EH/s, to put that number in perspective. Certainly, bitcoin’s price rebound was the big contributor to that hash rate growth and today at current prices, even Bitmain Antminer S17+ models from 2017 operating at 40.0 J/TH/s are above their breakeven prices (assuming $0.05 kWh power). As a reminder, bitcoin's hash rate grows in expectation of continued or growing mining profitability, achieved primarily through higher bitcoin prices as the network grows.

Hash Price Remains Resilient Despite Ramp in Hash Rate

The hash price, the dollars miners receive for their hash rate (daily miner revenue divided by network hash rate), remained resilient this year despite the massive ramp in network hash rate. Most of this was due to the increase in bitcoin’s price – hash rate grew 115%, but the price of bitcoin was up even more, 157%. On this basis alone, the hash price should have simplistically risen significantly. But the presence of prominent transaction fees is also contributing to growth in the hash price. Until the rise of BRC-20s in May of 2023, the transaction fee hash price was fairly low, $1-2/PH/s on average. But since creation of BRC-20s and with their renewed interested in 4Q, the hash price of transaction fees approached nearly $40/PH/s at one point. To put this in perspective, at the beginning of 2023, the total hash price, which mostly consisted of fees from the block subsidy, was only about $63/PH/s. At the end of 2023, the total hash price was about $91/PH/s, with $72/PH/s coming from the block subsidy and $19/PH/s coming from transaction fees. The increase in bitcoin’s price certainly helped hash price this year, but so did transaction fees.

Cleansing the Boogeymen of 2022

2023 was also the year that saw the resolution or near resolution of many of the calamitous the events of 2022. Do Kwon (LUNA/UST) was arrested, Sam Bankman-Fried (SBF) of FTX and Alameda was found guilty on all 7 criminal counts and Su Zhu of Three Arrows Capital was arrested (Kyle Davies is still wanted). Many of the notable companies of 2022, including FTX/Alameda, Genesis, Three Arrows, Celsius, Voyager, BlockFi, and Core Scientific, made significant progress on their bankruptcies or were resolved entirely. Even Mt Gox, which filed for bankruptcy in 2014, began to finally pay creditors back.

Also added to the list of bad actors was Changpeng Zhao (CZ) and his exchange Binance, both of which plead guilty to criminal violations, with CZ awaiting sentencing. Still outstanding are important civil cases such as the ones between the SEC and Coinbase and Binance, both of which might set the tone regulation in the industry for the years to come.

Crypto Linked-Equities Roar

If bitcoin’s quarterly and yearly returns were impressive, one has yet to look at what happened to crypto-linked equities. On a market cap basis, public Crypto Companies (varied companies, excluding miners) were up 121% in 4Q and 362% for the full year. Miners were up 106% in 4Q and 399% in 2023. To repeat what we have said in the past, crypto-related equities, especially miners, should have leveraged effects associated with the price of bitcoin. The reason is that when prices go up (or down), all the price change drops directly to the bottom line. There are no more incremental costs to mine bitcoin at $40,000 vs $35,000, keeping all other variables equal.

CME Bests Binance in Futures Open Interest

For several years now, Binance has been the place to trade crypto, both spot and derivatives. With the death of FTX last year, it looked like the exchange would have few challengers. But this quarter, the CME, a US regulated trading venue supplanted Binance, an unregulated offshore exchange, in terms of open interest on bitcoin futures. Trading volumes on Binance are still multiples of what they are on the CME, perhaps an illustration of the difference in investor bases, but we think the increasing open interest on CME speaks to a couple of things. First is the interest of US investors expressing long views, especially using the ProShares Bitcoin Strategy (BITO) ETF. The second is CTA and trend following funds, which buy bitcoin futures as they increase in price. Third is hedge funds and relative value funds, which engage in the basis trade of shorting futures trading at a premium to spot and short spot as a hedge. All of these have been sources of demand for futures in recent months.

Looking Ahead to 1Q24 and Beyond

ETF Decision Coming Any Moment

Depending on when this is read, a decision on the various ETFs, 13 by our count, may be rendered by the SEC. The overwhelming viewpoint, and one we espouse, is that the SEC will approve the listing exchanges’ (Nasdaq, NYSE Arca, and Cboe BZX) requests for a rule change, their 19b-4 filings. Again, this is a request by the exchange to list and trade this ETFs, and it is the overwhelming consensus view, but one that we agree with. The SEC can absolutely deny the requests, but it must do so using new reasons, ones not struck down already by the DC Court of Appeals. Furthermore, a denial, depending on its substance, could be challenged in court, like the Grayscale decision. Given how lopsided the court was in the Grayscale case (3-0), the SEC may not be so ready for another court battle. In addition, it would be a shock to have the SEC meet with issuers 28 times, mold their registration statements, and then deny them all. This isn’t out of the realm of possibility, but it seems uncharacteristic of a financial regulatory agency.

This decision could come any time, but is most likely some time between next Monday and Wednesday. Wednesday is the last day for a decision of the ETF with the first deadline, ARK 21Shares, and we think the SEC either approves or denies all the funds together, not playing favorites. Friday is a possibility, as the comment deadline for some of the ETFs end of the ETFs ends “by January 5th," but it seems unlikely the SEC would interrupt this process.

While it is perfectly rational to believe that the SEC will deny the ETFs (we don’t, but to each his own), a recent report from Asia-based OTC broker Matrixport doubting the ETF approvals roiled markets. Price dropped sharply, triggering over $100M in futures liquidations. On one hand, this highlights the lopsidedness of trader positioning heading into the decision. On the other hand, it highlights a persistent and pervasive issue in this industry, access to quality and thoughtful information. Again, we don’t take issue with the belief that the SEC is going to deny the ETFs, but the report itself contained no facts or sources, only opinions. The arguments these opinions rested on were barely cogent, made little sense from a readability standpoint, and showed a poor understanding of the innerworkings of the SEC. It got basic dates and facts wrong. We are not mincing words because the industry needs credible thought leadership and this piece, despite wide circulation, is not one of them.

Expectations Are Running High. Can They Be Met?

Circulating back to the positioning piece, investor expectations are clearly running high into the ETF decision deadline. Funding rates on bitcoin perpetual swaps hit a high of 96.5% (long were paying shorts 96.5% annualized interest rates) on an open interest weighted annualized basis is one example. The other is just the price appreciation since the appearance of the ETFs in mid-June.

We have shown the following analysis in the past, but it is worth revisiting. Since the appearance of the BlackRock iShares registration statement on June 15th, which touched off this entire ETF race, the price of bitcoin is up $16,668 and its market cap is up a whopping $339.6B (through end of December). Assuming all of that increase in market cap was a result of ETF anticipation (naïve we know) and a 10x money multiplier (for every $1 of capital that flows into bitcoin, its market cap goes up by $10), the market is expecting nearly $34B in AUM in the ETF. While that may happen over time (and thus would need to be discounted at an appropriate rate), it’s a significant hurdle, one that far surpasses the 1-year inflows of the GLD ETF of $5.3B, the most success ETF launch of all time (our figures are in 2023 dollars). In our opinion, $5.3B of inflows for the bitcoin ETFs would be an objective homerun, but clearly not what the market expects. We have seen numbers from prognosticators that clearly set a high bar - $15B, $50B, even $500B(?).

Where could our market implied ETF AUM number be too high and thus market expectations be more conservative? If one were to assume not all the price action since June were due to the ETF or if the money multiplier was higher than 10.0x (the commensurate number for stocks is 5x; the 118x number cited in a 2021 Bank of America report relied on ETF share issuance sensitivity – ETFs were not widely available then and thus we do not think it is a credible number). Regardless, this data plus the funding rate data paints a picture of high expectations.

Where could this flood of capital come from? One category of assets that should “donate” funds are the existing futures-based ETFs. While it is unlikely that they go to zero in AUM overnight, as they currently stand, they would be little need for them in a world where spot ETFs exists for US based investors. They have higher costs (BITO has a 0.95% management fee, while Fidelity’s spot ETF will have a 0.39% fee), have high roll costs associated with the contango (forwardation) shape of the futures curve (futures with expiries further out have higher prices) associated with financing costs, and higher tracking error to spot. The only time a futures-based ETF (as they currently stand) would be beneficial to investors is when the futures curve is in backwardation and the futures further out in expiry are trading below spot. This typically only happens in drawdowns (futures premiums/discounts are positively correlated with price). Of course, BITO also has been in the market for over 2 years and enjoys market acceptability and recognition, while spot ETFs would still be novel products. Regardless, we find comments like this from ProShares's Global Investment Strategist disingenuous and frankly, derogatory.

Again, this wouldn’t happen overnight, but there is over $1.8B of AUM currently invested in futures-based ETFs that could “donated” to spot ETFs in short order as investors switch to products with more favorable characteristics on nearly every level. We will only have to see when and if spot ETFs launch, which could happen within a week of 19b-4 approvals, as to how popular these funds are.

Basis Likely to Shrink, Maybe Permanently

The futures basis, the price differential between futures prices and spot, may be permanently altered following the launch of spot ETFs. A couple of factors are at play. One is lower demand for bitcoin futures, either through outright ownership or indirectly through the futures-based ETFs like BITO. Futures do give investors leverage that they may not be able to obtain through a spot ETF, but we would expect a spot ETF to have many advantages for the pure expression of bitcoin’s beta as previously discussed. One other factor is the ease of arbitrage. To engage in the basis trade today, investors have to put on 2 separate legs of the trade with 2 different service providers – shorting futures on the CME and buying spot bitcoin as a hedge (through an entity like NYDIG). That trade is not available or engaged upon by many traders. As a result, capital available for the arbitrage is limited and the basis can blow out to +30% on a gross annualized basis as it did a few days ago. When a spot ETF trades, it will be much easier for traditional market investors to put on the same trade, except replace the spot hedge against the short futures position with buying the ETF. The basis will likely still persist (and be positively correlated with price) but the highs and lows might be much more muted.

Halving on Deck in Mid-April

In mid-April, at block 840,000, one of the most noted events will happen for Bitcoin, a halving in the block subsidy, the incentive it pays the winning miner. On this date, estimated to be on April 11, the protocol will reduce the block subsidy from 6.25 bitcoins per block to 3.125 and reduce the annual supply growth from ~1.8% annually to ~0.9% annually (squarely below gold’s long term supply growth of 1-2%). This date keeps inching up and is less than the 4-year number that should be if blocks were exactly 10 minutes because hash rate keeps increasing during the 2,016 difficulty adjustment window.

This event is important for 2 reasons. First, halving the block subsidy is how Bitcoin achieves its (approximately) 21M bitcoins ceiling. Eventually, the block reward goes to 1 satoshi, the smallest divisible unit of a bitcoin, and then can no longer be divided in half. Second, historically, halvings have been a cyclical marker, bisecting cyclical peaks. Why has a violation of even the weakest form of the efficient market hypothesis (EMH), that past prices cannot predict future prices, persisted? Our best guess is that a combination of investor emotions, the fear and greed cycle, and heuristics, the availability of a price pattern that investors continue to repeat drawing. It is not, as some would have you believe, due to increasingly constrained new supply. At the halving, 450 fewer bitcoins will be created on a daily basis, which at $40,000 per bitcoin, amounts to only $18M. While lessening the daily selling pressure by $18M would certainly help price, it’s miniscule compared to the daily spot trading volume of bitcoin, which amounted to $4.5B daily on Binance and $783M on Coinbase in early January. Said differently, the daily supply overhang removal from the halving is a fraction of the daily trading volume of bitcoin.

One interesting note and word of caution is that we currently running well ahead of the recoveries from prior major price cycle drawdowns. This cycle, bitcoin’s price has recovered faster and further than in the previous 2 cycles. Perhaps this is because of a major catalyst, like the imminent ETF launch, that was not present in the prior cycles. While we don’t know exactly what is in store for bitcoin’s future price, this running ahead of prior cycles might be reason for a mid-cycle breather. One other interpretation is that that the last cycle high occurred in April of 2021 at $64,000, and it was the launch of BITO in November of 2021 that dragged spot to a new high (with futures trading at a +35% premium to spot at one point). Thus, we are much further into the cycle recovery than we would normally be. This is by no means a consensus view, but one we think is interesting.

Halving to Impact Miners, Transaction Fees to Lessen Blow

While miners had a good year in 2023, enjoying increasing hash price even as hash rate climbed, 2024 could bring about significant changes with the halving. A major portion of their revenue, the block subsidy, will be cut in half. That would’ve been a bigger problem before Ordinals and BRC-20s roared to life because the block subsidy accounted for ~98% of miner revenue. But as our hash price chart shows, fees count for an increasing portion of miner revenue. If fees stay high, that should lessen the blow felt by miners. Price appreciation has done a lot of heavy lifting as well, and as a result, even very old mining rigs are above their breakeven prices. Given these conditions, we would expect to see miners continue to add hash rate throughout 2024. If the pace of ~23 EH/s/month is continued, we would end 2024 with a hash rate of 800 EH/s.

Regulatory and Legislative Developments

On the regulatory and legislative side, there are a couple of things we are tracking. In the SEC case against Coinbase, it isn't crazy to think the court could throw out the case around the end of Q1. If the judge decides to wait for summary judgement motions, it might push things out a year or so. Ultimately, the case could very well end up in the Supreme Court (with Coinbase as the favorite in our opinion). The SEC’s silence on Ethereum as a security paved the way for ETH based futures ETFs, which have gathered a paltry $51M in collective AUM, and now potentially spot ETFs sometime later this year. The SEC may not yet be done with enforcement actions, however, as we would not be surprised to see further actions against centralized exchanges or even DeFi platforms. On the legislative side, we would hope to see progress on the stablecoin and market structure legislation, but we are not hopeful for more encompassing digital asset legislation in an election year.