IN TODAY'S ISSUE:

- Bitcoin Core 26.0 is released, reminding us of what Bitcoin is and isn’t.

- Critics often point to Bitcoin’s shortcomings without greater context or appreciation of what drives demand or value.

- Bitcoin ultimately has value because of the social agreement between its users, who may appreciate it for the technical properties of the software or the risk and return profile of the asset.

New Release Reminds Us of What Bitcoin Is and Isn’t

This week saw the release of Bitcoin Core 26.0, ushering in a new version of “Bitcoin.” While the Bitcoin ecosystem at large consists of numerous pieces of software that interoperate (wallets, mining software, Lightning, alternative implementations of Bitcoin written in languages other than C++, etc.), Bitcoin Core is typically the most important because of its popularity and it de facto defines the broader Bitcoin protocol with which other pieces of software interoperate. While most of the technical changes in the recent version could be described as evolutionary rather than revolutionary, it is important to remind investors, especially given the resurgence in price (and criticism), of what Bitcoin is and isn’t.

Bitcoin is Software

At the risk oversimplification, Bitcoin (big “B”) is a software program, one that is freely available to anyone with an internet connection and a computer to download and run. Version 26.0 is available here. The individuals and organizations that run this software form a peer-to-peer network, one that is global in its reach, does not rely on any single entity like a financial institution or cloud service provider, and is difficult, if not impossible, to block (censor). The technical requirements are modest such that nearly anyone with a modern computer should be able to run it. By one measure, there are 67,000 Bitcoin Core nodes (software instances) currently being run. This omits important network participants such as miners, wallets owners, and exchanges, but we are going for simplification here – plus Bitcoin Core incorporates all of that functionality, as well.

Bitcoin is a Network

This system, the network of software, allows participants to send, receive, and hold bitcoins, the native asset endogenous to the system. It also allows users to verify and append new transactions between users. These bitcoins don’t live in your wallet. They reside on every computer in the network in a shared and ever-growing database called the blockchain. The keys (password) are secured in a wallet that gives its owner the right to reach out into this network and move certain bitcoins from one owner to another (along with encoding other information as is increasingly popular). That’s it. In that sense, the original white paper described it best – Bitcoin: A Peer-to-Peer Electronic Cash System.

Bitcoin is an Asset

Ownership of the bitcoin (little “b”) asset, unlike stocks or bonds, confers no rights to its owners. Bitcoins produce no cash flow and does not give a voting say in the development of the software. The only right bitcoin ownership confers is the right to move them. Because of this, many critics say that there is no inherent value and there is nothing backing it. To this we say, think harder, just a little bit.

First off, there are plenty of assets that investors hold that produce no cash flow, even in the theoretical construct – precious metals (gold, silver, platinum), art, collectibles (automobiles, watches, jewelry, handbags, fine wines) are just some of them. How did Michael Saylor/MicroStrategy come back into contact with Bitcoin after initial skepticism? A website (voice.com), another non-income producing asset, was sold to Block.one (creator of EOS) for $30M. Assets do not need to have cash flow for them to have value or be valuable.

Second off, even for assets that are theoretically backed by cash flows, equities for example, the practice of discounting cash flows may be of little (or negative) value. Discounted cash flows and dividend discount models are just that, models, and “all models are wrong, some are useful,” the saying goes.

One only has to go back to 2014’s “Great Debate” over Uber’s valuation between the “Dean of Valuations,” NYU professor Aswath Damodaron and VC legend, Benchmark’s Bill Gurley to illustrate the point. Damodaron had (thoroughly) valued the company at $5.9B following its $17B round, while Gurley claimed that Damodaron’s total addressable market (TAM) was off by a factor of 25, thus undervaluing the company. Who won the debate? Today, nearly 10 years later, Uber’s enterprise value is $131B enterprise value. And Uber still hasn’t produced positive free cash flow (as of fiscal year end 2022) on an annual basis. You decide.

As an aside, bitcoin is a monetary base, not a stock, bond, real estate or company. One should not expect a monetary base to produce cash flow (even US dollars have to be invested to generate a return). Comparing bitcoin with these other asset classes is like comparing apples and oranges.

Investing in Non-Income Producing Assets

Why do investors own non-income producing assets? Either for objective reasons (returns and risk characteristics), subjective reasons (they enjoy the art), or both. While there might be subjective reasons for owning bitcoin (social media status, group alignment with political/economic beliefs), we would guess that most of the value in bitcoin ownership comes down to objective reasons (risk diversifier, return profile, globally transmissible, nearly infinite divisibility, and weightless in its cost to transport). Much of that objective value comes from technical properties, but there are important subjective properties as well.

It should be of little debate that Bitcoin has a programmatic supply function, one that is halved roughly every four years until it is exhausted at nearly (not exactly) 21 million bitcoins. Again, this happens for a technical reason – eventually the block reward can no longer be divided in half. But whether a fixed supply is valuable is complicated subject.

We’ll start off with the simple observation that not all things that are scarce are valuable. If one were to rank the minerals in the earth’s crust by scarcity, it would not match with its value on a price on per unit of weight basis. Why? There simply might not be demand for a mineral, no matter how scarce it is. The same logic goes for the cost of production. Just because something is costly to produce, does not automatically confer value to it. That again, comes from demand. When something is both costly (time, money, resources) to produce and it is highly demanded, then something special happens.

Consumptive vs Subjective Demand

What drives demand? Some minerals are consumptive and used as inputs in economically sensitive processes or goods, like copper. In the context of Bitcoin, one might consider transactional demand, the transmission of bitcoin in exchange for goods and services, as a source of consumptive demand. That’s still very much a work in progress as bitcoin is still not widely used as a medium of exchange or unit of account.

Demand for other minerals could be considered driven by subjective factors – gold, silver, platinum, palladium (yes, there are industrial applications for these minerals, as well, but that only accounts for 7% of gold demand for example), as well as precious gems, like diamonds, rubies, and sapphires. What drives subjective demand? Social agreement. An individual may prefer rubies over diamonds, but society at large values diamonds more, making them more valuable. In that sense, subjective value is a social construct – the more people that value something, the more valuable it should be.

Counter to the Counterfeiting Argument

A common critique of Bitcoin is that it is easily copyable. It is, after all, open-source software. Indeed, Bitcoin has been copied many times and changed, sometimes in trivial manners. But just because it can be copied doesn’t mean the value of Bitcoin is any less. Again, this value comes from the social layer, an agreement of what “Bitcoin” is by its users. Simply copying the code and making a few changes is unlikely to generate much change in the social acceptance of Bitcoin and therefore is not detrimental its value.

Bitcoin Doesn’t Care

When someone criticizes Bitcoin, do they think it cares? It can’t. It’s a computer program. It simply executes the code that has been written. It has no religion, political allegiance, or national identity. It doesn’t even know what the price of bitcoin is. When critics level complaints about Bitcoin/bitcoin (“you’re not even used as a medium of exchange, you produce no cash flow, you’re too volatile”), it responds with a resounding silence.

What does have those attributes, though? People, some of whom utilize or maintain Bitcoin, but many of whom do not. And while certain beliefs may be common across the Bitcoin community, it is far from a monolith. But the one thing that seems to be certain that the critics can’t understand is that Bitcoin is valuable, and bitcoin has value.

Market Update

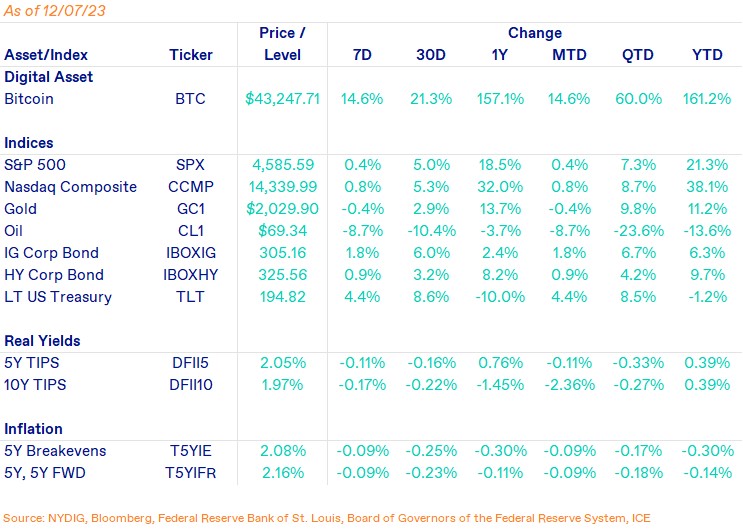

Bitcoin continued its upward trajectory this week, zooming up 14.6% on the week. Bitcoin seemed to make short work of “even level” price resistance, punching through $40K without much effort. At its highest point this week, bitcoin touched $45K. The asset is now up 161.2% on the year, a stark contrast of where it was at this point a year ago. Equities were up on the week, although clearly unable to keep pace with bitcoin. The S&P 500 was up 0.4% while the Nasdaq Composite was up 0.8%. Bonds rallied as well with investment grade corporate bonds up 1.8%, high yield corporate bonds up 0.9% and long term US Treasuries up a 4.4%. Please note that we have switched to total returns analysis instead of a pure ETF price/index level analysis for stocks and bonds. Gold fell 0.4% following abnormal trading over the weekend that saw a significant rise and then fall. Oil cratered 8.7% on increasing supply from the US.

Important News This Week

Investing:

Bitcoin Price Hits $42,000 as Crypto Rallies; Ether, Dogecoin Gain - Bloomberg

SEC Filings That Mention Bitcoin Surged to Record High Last Month - The Block

Bitcoin Price Could Potentially Rise Above $50,000 in early 2024: CryptoQuant - The Block

Meanwhile Group Unveils First Bitcoin Private Credit Fund - Meanwhile Group

Bitcoin is Earning Its Place in a Balanced Portfolio - Bloomberg

Bitcoin From Satoshi Nakamoto's Era Were Moved as BTC Prices Hit $44,000 - CoinDesk

US Bitcoin ETF Issuer Talks with SEC Have Advanced to Key Details -Sources - Reuters

Regulation and Taxation:

Founder and Majority Owner of Cryptocurrency Exchange Pleads Guilty to Unlicensed Money Transmitting - DOJ

US Judge Bans Changpeng ‘CZ’ Zhao from Leaving the Country - Decrypt

US Crypto Industry Lobby Spending on Track for New Record in 2023 - Reuters

Companies:

Bitcoin Staking Protocol Closes $18M Round Led by Polychain and Hack VC - Blockworks

Technology:

Bitcoin Core's 'v26.0' Upgrade Aims to Impede Eavesdropping, Tampering - CoinDesk

Jack Dorsey Leads Seed Round in Support of OCEAN'S Mission to Decentralize Bitcoin Mining Globally - OCEAN

Upcoming Events

Dec 12 - November CPI release

Dec 13 - FOMC interest rate decision

Jan 5 - Comment rebuttal deadline for Franklin, Hashdex ETFs

Jan 10 - Final ETF decision deadline for the first bitcoin ETF, ARK 21Shares