IN TODAY'S ISSUE:

- As turmoil spills from traditional markets into crypto, we look at what the data says about bitcoin’s use as “digital gold”.

- Our updated and expanded analysis again does not show that bitcoin is an effective hedge against sharp drawdowns in the stock market (neither is gold), but bitcoin really shines in the recovery phase.

- Bitcoin has historically thrived amidst geopolitical unrest, as any erosion of societal confidence, whether gradual or abrupt, has only served to bolster the asset.

Asset Returns in Risk Off Environments

Monday kicked off the week with a tumultuous start as both the S&P 500 and the tech-heavy Nasdaq Composite experienced their worst trading sessions since 2022. The S&P 500 began the day down 4.3%, while the Nasdaq Composite opened the day down by 6.4% before eventually closing at 3.0% and 3.4% lower, respectively. At one point during the day, the VIX (Cboe Volatility Index) surged above 65, a level seen only twice before, once during the COVID-19 crisis and again during the Global Financial Crisis. Although markets have now recovered from Monday’s sell-off, the trading activity appears to be the extension of a longer risk-off trend that started after the market peaked in mid-July.

Bitcoin and the larger digital asset ecosystem were not immune, as the volatility in traditional markets spilled over into the digital asset markets. With bitcoin experiencing a steep drop over the weekend and again on Monday before recovering, many began to question bitcoin’s role as “digital gold” or a “store of value”. Bloomberg journalist Joe Wiesenthal called bitcoin “three tech stocks in a trench coat” (ok, points for humor) while Nassim Nicholas Taleb engaged in a spirited debate with the hosts on CNBC.

It has been some time since we performed this analysis, almost three years, and a lot of things have changed in financial and crypto markets. But given the recent market action and some misunderstandings about bitcoin’s behavior as a financial asset, we think it is time to revisit our analysis.

Numbers, Not Narratives

To start, terms like "digital gold" and "store of value" are often used to describe bitcoin's purpose or potential applications, something the community of investors and users have given it. However, Bitcoin espouses none of these narratives. It functions as a "peer-to-peer electronic cash system", enabling users to hold, send, and receive bitcoins, a fixed supply digital asset native to the system. Bitcoin is also highly liquid in secondary trading markets that are active 24/7/365. By observing how bitcoin's price behaves in specific situations, however, such as significant selloffs, we can gauge investors' attitudes towards the asset. This approach allows us to let the data shape the narrative, rather than the other way around.

Looking at the Biggest Single Day Drops in the Stock Market

By analyzing bitcoin’s performance during times of market stress, defined as declines in major stock market indices, we can better ascertain what investors are doing with their bitcoin investments. We can also compare that performance to that of gold and long-term US Treasuries, other assets that investors might seek in times of stress. We do this first by looking at the biggest 1-day declines in the S&P 500 Total Return Index (SPXT) as defined by 3-sigma (standard deviation) downward moves in the value of the SPXT (our analysis begins in 2011). Then by looking at aggregate data on gold, long-term US Treasuries, and bitcoin, we can make some conclusions. As an aside, Monday's 3.0% daily drop didn't even make this list.

One key takeaway from the data is the reliability of US Treasuries as a safe haven during stock market downturns. Long-Term US Treasuries have a negative correlation with major S&P 500 drops (-0.27), with an average increase of +0.74% (which may not fully protect a 60/40 portfolio), and have gained in value nearly 72% of the time (win rate). In contrast, gold has a minimal average return (+0.01%), is positively correlated with stock market declines (+0.59), and shows positive returns just over half the time (56.25%). From our perspective, gold is a less effective hedge compared to long-term US Treasuries. When it comes to bitcoin, however, there is scant evidence that it serves as a hedge during significant 1-day stock market declines. Bitcoin demonstrates negative average returns, a low win rate, and a positive but weak correlation. While bitcoin may offer some hedging benefits, it appears to be geared towards risks other than sharp S&P 500 drawdowns.

What About Longer Drawdowns?

We looked a 1-day drawdowns, but what about multi-day drawdowns? Here we look at all the drawdowns experienced by the S&P 500 of greater than 5% since the beginning of 2011, including the most recent drawdown. While the timelines are longer, the conclusions are largely the same. Gold is an unreliable hedge while long-term US Treasuries are the better hedge on all metrics. Bitcoin again fares similarly as with 1-day drawdown. It does, however, drop much less than the S&P 500, although with a much wider standard deviation.

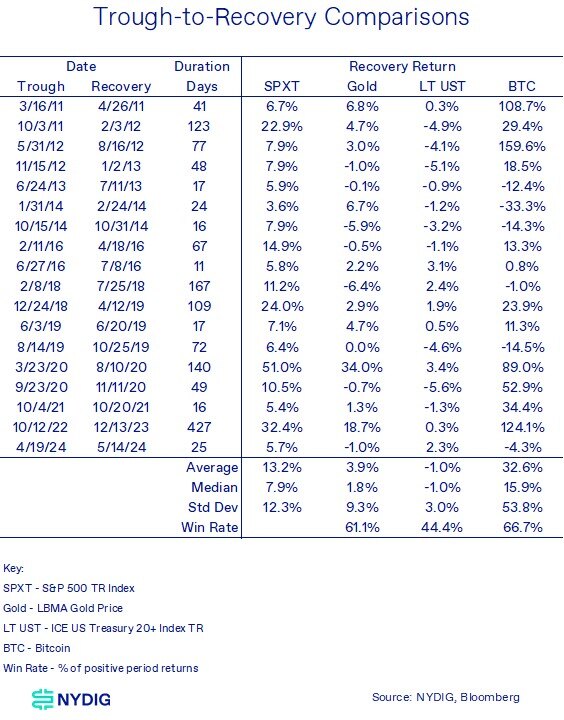

Bitcoin Shines in the Recovery Phase

As bitcoin may not shield against stock market selloffs, what about its potential during the recovery phase? Bitcoin truly shines in this phase. The table below highlights the impressive performance of bitcoin in recovering from market lows back to previous highs after a downturn in the S&P 500. Meanwhile, traditional assets like gold show positive returns, while long-term US Treasuries experience a decline.

Parting Thoughts

Investors, individuals, and corporations face a wide array of risks, whether they are aware of them or not. Even storing your money under the mattress or in a bank account carries risks such as inflation, bank counterparty risks, or theft. Our focus here is on a very specific risk, a decline in the S&P 500. While these declines can stem from various factors, our analysis reveals that long-term US Treasuries offer the most reliable protection against this type of risk. However, even if an investor follows the traditional 60/40 (stocks/bonds) portfolio, the increase in Treasuries may not fully offset the losses experienced in the stock portion of the portfolio.

Our updated analysis once again highlights that bitcoin may not be the ideal hedge against sudden stock market shocks and gold is far from perfect. Our theory is that the high liquidity of bitcoin allows investors to express their opinions beyond traditional market hours (the recent price movements over the weekend were quite revealing). It is important to keep in mind that bitcoin's correlations and price fluctuations are merely reflections of collective human behavior, rather than inherent characteristics of the asset itself. Bitcoin as a financial asset only has the characteristics that we impute on it.

Where has bitcoin has shined, however, is during geopolitical turmoil, when trust in the institutions around us is lost. We see this with specific events around the world, something we’ve analyzed in previous research. One can also think the longer arc of declining trust in institutions over the past few decades as one that plays to bitcoin’s strength. With that in mind, there's one bitcoin adage that applies: don't trust, verify.

Market Update

Bitcoin was down 6.1% this week as contagion from traditional financial markets spilled into crypto markets. Bitcoin hit a low of $49,050 on Monday morning, but rebounded throughout the week, ultimately breaking back above $60K.

Despite the drawdown in bitcoin price, which was at $70K just a week earlier, trading looked orderly and few edge cases that we sometimes see in extreme conditions emerged. Long bitcoin futures liquidations hit $380M over the weekend, a big number, but nowhere near a peak event like the Black Thursday selloff during COVID ($1.7B). Stablecoins mostly held their value, with some wobbling in Tether ahead of last weekend that was corrected by the end of day on Sunday.

Perpetual swaps and futures did not trade to sharp discounts to spot, and the basis on front month CME contracts compressed, but has held at mid-single digit levels. The spot ETFs started Monday trading at discounts to NAV (10 – 25 bps) but sharply recovered along with spot as the day went on. The bitcoin ETFs posted outflows of $168M on Monday. Finally, in a sign that much of the speculative exuberance has left the market, memecoins DOGE and SHIB have now almost entirely roundtripped the price bump they received in February and March.

Important News This Week

Investing:

Jump Crypto Moves Hundreds of Millions in Crypto as Prices Slide - The Block

Bitcoin Institutional Adoption 'Remains on Track' Despite Market Turbulence: Bernstein - Decrypt

Cboe Re-Files for Spot Bitcoin ETF Options in Sign SEC May Be Engaging: Analysts - The Block

Regulation and Taxation:

Crypto-Friendly Bank Ordered by U.S. Federal Reserve to Limit Risks from Digital Asset Clients - CoinDesk

Putin Signs Law on Legalizing Cryptocurrency Mining in Russia - TASS

XRP Jumps 17%, Beating Bitcoin Gains, as Ripple-SEC Case Ends - CoinDesk

Judge Approves $12.7 Billion Settlement Between FTX And CFTC, Bringing 20-Month-Long Lawsuit to An End - The Block

Companies:

Bitcoin Strategy of Michael Saylor Factored in Eric Semler's Actions - CoinDesk

Japan’s Metaplanet Takes $6.8 Million Loan to Buy More Bitcoin - The Block

Path Taps Gemini as Custodian for New Automated Crypto Portfolio App - The Block

Ionic Digital Issues Shareholder Update - Iconic Digital

Upcoming Events

Aug 14 - August CPI reading

Aug 22 - Jackson Hole conference

Aug 30 - CME expiry