SECOND QUARTER 2021 REVIEW

We look back at the second quarter and the events that shaped it, as well as look forward to important events in the future.

QUICK TAKEAWAYS:

2Q21 Marks One of Bitcoin’s Toughest Quarters

Bitcoin had a tough second quarter, finishing the period down 40.7%. This not only makes 2Q21 one of bitcoin’s weakest performing quarters since 2011 but also its weakest second quarter ever. The second quarter has historically been a period of strong returns, with only two prior second quarters showing negative returns, reminding us that past performance is not indicative of future performance.

Quarter Comes of the Heels of Very Strong Performance

When contextualizing the weak performance in 2Q21, we think it is important for investors to keep in mind the recent performance of bitcoin. Even though bitcoin was down 40.7% in the quarter, it had just come off four consecutive quarters of strong performance. Given this string of winning quarters, we do not find it surprising that investors used the period to realize gains.

Bitcoin is Still One of the Best Performing Assets Classes of 2021

Despite the tough second quarter, bitcoin is still up 19.1% year-to-date, making it one of the best performing asset classes of 2021 to date. Performance is now more in line with traditional asset classes, but bitcoin still ranks #6 of all asset classes outlined below.

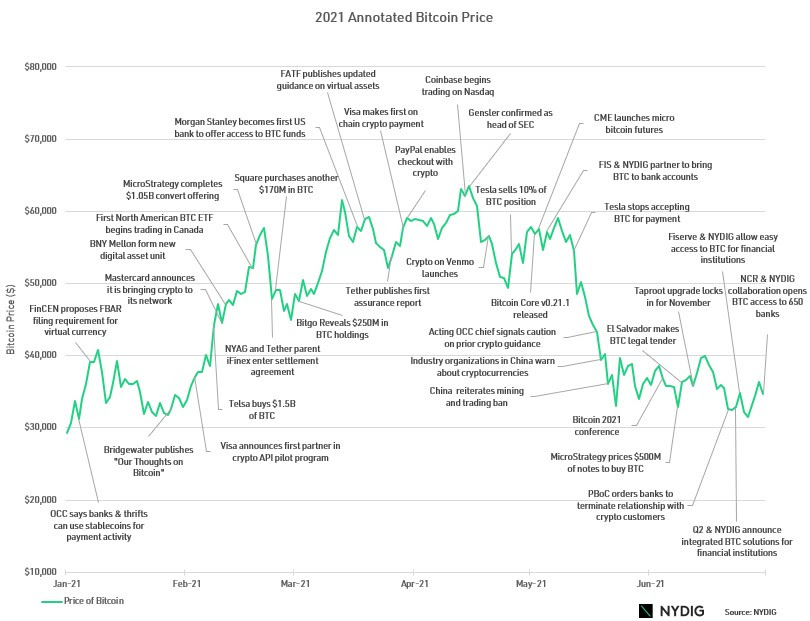

News Headlines Dominate the Quarter

Bitcoin and the ecosystem had several positive items during the quarter. El Salvador became the first nation to accept bitcoin as legal payment, the most significant technology upgrade in four years, Taproot, was approved by miners and will go into effect in November, and numerous banks and bank technology providers, including Alkami, FIS, Fiserv, NCR, and Q2, are working to enable access to bitcoin through traditional banking venues. On the flip side, Tesla’s about-face in accepting bitcoin for payment, increasing environmental concerns regarding mining, and China’s crackdown on trading and mining weighed heavily on bitcoin during the quarter. We continue to think the elimination of the China overhang will ultimately be good for bitcoin and migration of hash power out of China allows the industry to make bitcoin mining greener and more efficient.

Electricity Consumption Drops Amidst Hash Rate Reduction

Bitcoin’s declining hash rate amidst the China mining crackdown was one of the most widely discussed topics during the quarter. With nearly a 70% reduction from the peak so far, bitcoin’s hash rate underwent a severe correction as China made a push to shut off mining in every major province. While it remains to be seen where or when that hash rate comes back online, along with the reduction in the hash rate came a swift reduction in electricity consumption. Data from the Cambridge Centre for Alternative Finance indicates that electricity consumption is down 55% from the peak of 143.9 TWh to 64.7 TWh at the end of June. Investors should rest easy that even though the hash rate has come down, bitcoin is still very secure and bi-weekly difficulty adjustment ensures that blocks continue to be produced at regular intervals.

Bitcoin Dominance Fluctuates

Throughout the quarter, we received numerous questions about bitcoin's “dominance,” its market cap as a percentage of the overall industry market cap. Dominance can be a noisy signal as the denominator in the measurement, the size of the industry market cap is not stable in terms of the number of constituents. The cryptocurrency industry is secularly growing, and new assets are created, launched, or come into existence daily. This makes comparing dominance levels from cycle to cycle a challenge, but we do think there is some information to glean about cycles and investor preferences from the change in dominance. The following graph highlights some important markers in the history of bitcoin dominance.

- Bitcoin dominance took its first steep drop in spring 2017, amidst the rise of Ethereum and sudden overnight retail frenzy for alts (alternative currencies), like Litecoin and XRP.

- Dominance hit a local low in mid-2017 as the Initial Coin Offerings (ICOs) peaked, and bitcoin struggled ahead of the Bitcoin Cash fork.

- With the Bitcoin Cash fork behind it, bitcoin rallied into year-end, peaking in price in mid-December.

- Bitcoin dominance hits a cycle low in mid-January 2018, as Ethereum prices reached their cyclical peak nearly a month after bitcoin.

- During the 2018 drawdown, bitcoin regains dominance as alts fall more than bitcoin, proving their riskiness during the risk-off environment.

- Bitcoin continues to rally in 2019, gaining dominance, as the asset is up over 90%, while major alts like Ethereum end the year down.

- Bitcoin dominance breaks through 70% in early January 2021 amidst stellar performance throughout 2020.

- Bitcoin dominance drops below 40% for the first time in the cycle, as price consolidates while alts rally.

- Bitcoin regains dominance during the May and June market correction.

Looking Ahead

With the difficult 2Q21 behind us now, we think it’s important to look ahead to some of the events that we think will shape the coming months and quarters. On July 21st, Elon Musk and Jack Dorsey will have “the talk” at The B Word conference hosted by The Council for Crypto Innovation, Ark Invest, Square, and the well-respected VC firm Paradigm. Presumably “the talk” centers on Bitcoin’s energy consumption, an issue that Musk has aired many times online and the primary reason Tesla stopped accepting bitcoin for payment. Taproot, the most significant technical update to Bitcoin since 2017, will be activated on block 709,632 sometime in mid-November. The growing adoption of bitcoin as a financial asset by institutional investors continues, with names of new well-respected investors in the news regularly. Numerous bitcoin ETF applications continue to work through the SEC process. Finally, the activation of millions of potential bitcoin customers through traditional banks and financial institutions is underway thanks to the efforts of our organization and our banking and technology partners. To us, the secular growth case for the asset has never been clearer.Thanks for joining us again this week. Please reach out with any questions or comments.

Sincerely,

GREG CIPOLARO

GLOBAL HEAD OF RESEARCH

This report has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This report does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (“NYDIG”).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein in managing client accounts. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this report.

There can be no assurance that any investment strategy or technique will be successful. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment, which may differ materially, and should not be relied upon as such. Target or recommended allocations contained herein are subject to change. There is no assurance that such allocations will produce the desired results. The investment strategies, techniques or philosophies discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this report may contain forward-looking statements regarding future events, targets, or expectations regarding the strategies, techniques or investment philosophies described herein. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this report, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this report are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. Before deciding to proceed with any investment, investors should review all relevant investment considerations and consult with their own advisors. Any decision to invest should be made solely in reliance upon the definitive offering documents for the investment. NYDIG shall have no liability to any third party in respect of this report or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this report in its entirety, the recipient acknowledges its understanding and acceptance of the foregoing terms.