IN TODAY'S ISSUE:

- A rise in ETH price and trading activity has led to a broad discussion regarding a market cap “flippening” with BTC.

- ETH options trading has increased, especially upside call options.

- However, a closer observation of options trading data complicates this bullish story.

Is the "Flippening" on the Horizon?

Over the past few weeks, numerous media outlets and crypto community members have pointed to a surge in ether options as a sign that the “flippening” — crypto jargon for a potential event in which ether (ETH) unseats bitcoin (BTC) as the largest cryptocurrency by market cap — is upon us. This commentary has been accompanied by surging options activity in advance of “The Merge,” a significant technical update to the Ethereum network. However, a closer inspection of trade data shows that, while traders appear to be expressing bullish views, it is not as unbridled as a cursory analysis of the data might suggest.

Some Background First

Bitcoin, the progenitor of the digital asset class, has never been topped by any other cryptocurrency in terms of size at any point in its history. The initial coin offering (ICO) craze of 2017, which was almost entirely centered on Ethereum, drove ETH’s market cap to a peak of 83.5% of BTC, but that was short lived. In the ensuing drawdown of 2018, ETH’s market cap receded relative to BTC, being briefly overtaken by another token, XRP. Aside from that brief period, though, ETH has held a consistent number two position behind BTC. Today, ETH sits at about 45% the size of bitcoin’s market cap, wit

Ethereum is on the verge of a long-awaited major protocol update dubbed “The Merge.” The Merge is designed to jettison Ethereum’s existing Proof of Work consensus system, which is similar to that of Bitcoin, in favor of a relatively new mechanism called Proof of Stake. A protocol's consensus mechanism is crucial for keeping in sync the many computers around the world that collectively run the network. Changing it, therefore, is not something undertaken lightly. It is like changing the engine of an airplane while it is flying.

We will not delve into the details of Ethereum’s transition to Proof of Stake here, but readers should be aware that this is one of the most watched and most debated updates across the entire digital asset landscape to date, certainly since Bitcoin’s SegWit debate in 2017, but perhaps ever. It has serious economic and technical implications, and its development has taken years and has been marked by numerous delays. But, finally, during the week of September 19th, The Merge may be coming.

Options Traders Play the Merge

The news of a more precise timeline for The Merge was outlined on a call with Ethereum developers on July 14, which sparked a rally in the spot price of ETH. Concurrent to the jump in spot, trading activity in options also increased, particularly in relation to BTC, suggesting that traders were beginning to position themselves in anticipation of this momentous event. ETH option volume — which is generally around 60% of the total daily notional trading volume (in U.S. dollars) of BTC — began to overtake that of BTC. The rise in trading activity led to an increase in open interest, the value of outstanding options contracts, which also surpassed that of BTC on July 23.

Put to Call Ratio Shows an Increase in Call Activity

With the recent rise in ETH trading, we think it is instructive to peel back the onion and determine what traders are doing. One popular options metric is the ratio of the number of put contracts traded to the number of call contracts traded — the put-to-call ratio. Given that calls allow for traders to express leveraged long views, a declining put-to-call ratio is sometimes viewed as a bullish signal. Indeed, the put-to-call ratio has been steadily declining since mid-year and took a big leg down in July. This makes sense if traders view The Merge as a favorable event for Ethereum, but, as we discuss later, looking at call option volume alone does not tell the full story.

Expiration Dates May Hold Clues to Event Path

Most of the (mostly call) option contracts outstanding expire at the end of September 2022, December 2022, and March 2023, with the majority expiring in December. The build-up of call contracts expiring in December is notable given that The Merge is tentatively slated for mid-September. This may imply that traders expect a prolonged rally following The Merge or that they think it could be delayed. For comparison, open interest in December BTC options is roughly the same for its September and December expirations, with a much smaller amount in March 2023.

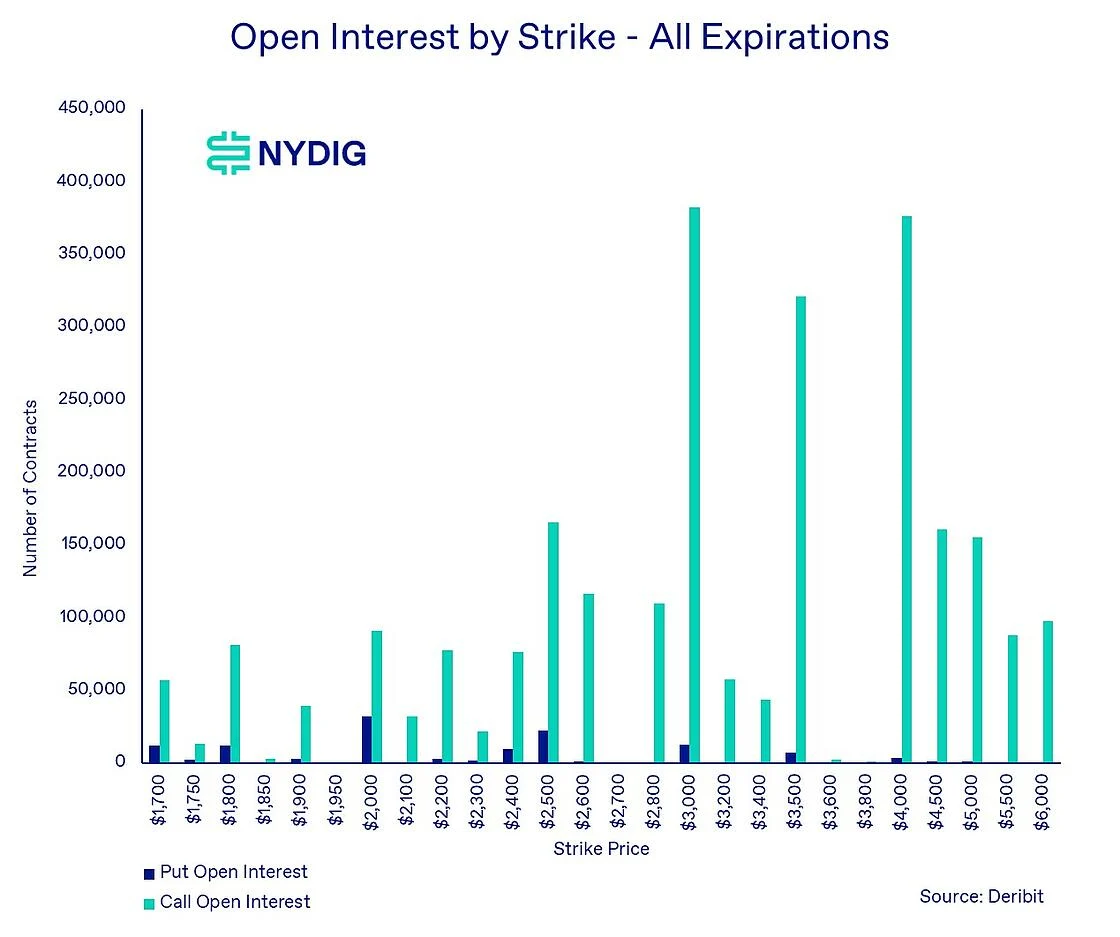

Out-of-the-Money Calls Show Important Price Levels

ETH options’ open interest shows a pronounced build-up of call contracts at the $2,500, $3,000, $3,500, and $4,000 strike prices (vs. current spot price of $1,591). More specifically, the $3,000 strike calls expiring Dec (320K contracts) account for a large portion of the contracts expiring in December. These price levels are important because they illustrate key price levels that traders and market makers are eying over the upcoming months.

Public Analysis Misses the Marks

Journalistic outlets and social media have been quick to pick up on the growing option activity for ETH, concluding that traders are wildly bullish ahead of The Merge and that ETH has “flippened” BTC in terms of options activity. That said, there is an important nuance to the analysis of trade activity that is missed here, which is that traders can sell calls as well as buy them. Call options represent the right to buy the underlying asset, in this case ETH, at a specific price up to a specific time. Buying a call can be a way for a trader to express a directional view without the capital outlay of buying the same exposure in spot. When trades are executed on an exchange like Deribit, which represents over 90% of the options trading volume, each transaction is are marked as either a “buy” or a “sell.” This may seem odd, as all trades involve both a buy and a sell simultaneously. However, based on the price a trade is executed and the order book, it can be inferred whether the initiator of a trade aimed to buy or sell the option. Trades executed at the offer price imply that an active trader is expressing a market opinion by buying from a market maker who is simply trying to make money by providing liquidity. Thus a trade is marked a “buy” when it is executed on the offer, or ask, side of the market, while it is marked a “sell” when executed on the bid side of the market.

If all we saw in trading activity was call ”buys,” we would have a similar conclusion to media outlets, that traders are wildly bullish about The Merge. In reality, however, the data shows a lot of call selling in addition to buying, which still results in the growth in trading volume and open interest but is a very different trade. Based on data from Deribit, it appears that the market is, in aggregate, roughly executing what is known as a “butterfly” options strategy on the upside. This means that traders are buying calls around the $2,500 strike, selling double that amount of calls around the $3,000 strike, and buying again around $3,500. This means that they profit if ETH prices increase, but only if prices increase to less than $3,500, otherwise they get nothing. This is a cheaper trade than purely purchasing upside, as this options structure is 1/3 the price of just buying the $2,500 call. With this $3,500 strike price more than double today’s spot price of $1,591, traders clearly see upside, but not unlimited upside.

Conclusion

The consensus view in public media outlets, that trades appear to be very bullish ETH leading into The Merge, certainly has merit. Traders are indeed purchasing upside call options to take advantage of a potential price spike. However, the degree of bullishness is likely overstated. Much of the open interest is associated with larger option packages that exhibit more nuanced views on prices. We will continue to closely watch positioning in the coming weeks as we approach The Merge.

Bitcoin fell 5.7%, following a couple weeks of gains. Equities gained, as the S&P 500 rose 2.0%, and the Nasdaq increased 4.6 %. Bonds also gained: Investment Grade Corporate Bonds were up 0.4%, High Yield Corporate Bonds rose 1.0%, and Long-Term Treasuries gained 1.5%. Gold increased by 1.7% on the week as real yields increased and inflation expectations decreased.

Important News This Week

Investing

Coinbase to Offer Crypto through Blackrock's Aladdin — Coinbase

Brevan Howard Scores Largest Crypto Hedge Fund Launch Ever — Blockworks

Key Ethereum Miner Pushes for Fork — The Block

ETHPoW vs ETH2 — BitMEX

Virginia Pension Invests in Crypto Lending — Financial Times

North Korean Crypto Job Search Scam — Bloomberg

Chainalysis Reports on Bridge Protocol Hacks — Chainalysis

CME to Launch Euro-Denominated Bitcoin and Ether Futures — CME

Regulation and Taxation

New Bill Aims to Give More Power over Crypto to CFTC — Bloomberg

FDIC Reminds Consumers that Crypto Deposits are Uninsured — FDIC

Binance.US to Delist AMP After SEC Security Claim — CoinDesk

New York AG Seeks Crypto Whistleblowers — The Block

SEC Charges Forsage Founders, Promoters — The Block

Companies

Saylor Assumes Executive Chairman Role at MicroStrategy — MicroStrategy

Vauld Gets Three-Month Moratorium Extension — The Block

Ledger Seeks New Funding at Higher Valuation — Bloomberg

Binance Pushes Back on AML Criticism — CoinDesk

Point72’s Steve Cohen Exits Radkl Investment — Bloomberg

Robinhood Crypto Unit Fined $30 Million — Bloomberg

Robinhood Cuts 23% of Staff — Robinhood

Upcoming Events

August 10th – July CPI data is released

August 26th – CME bitcoin futures and options expiry

September 2nd – United States Non-Farm Payrolls

September 21st – Next FOMC interest rate decision

Thanks for joining us again this week. Please reach out with any questions or comments.

Sincerely,

The NYDIG Team