IN TODAY'S ISSUE:

- The Friday anomaly appears to be back in force amidst the recent rally

- What growth in Tether supply says about the current rally

- Our analysis does not show that trading on Binance has been leading the rally

Friday I'm in Love, Again

Nearly 2 years ago, we published a report exploring the strange anomaly of day-of-the-week returns. Our analysis identified Fridays as the day of the week by far and away with the highest returns. While we have numerous theories for the anomaly, closure of the fiat banking system over the weekend, fund subscriptions, and derivatives expiry, none of the proposed explanations felt entirely satisfactory.

Since the Friday anomaly peaked around bitcoin's all-time high set over a year ago, Fridays have been a drag on performance, until recently. With the recent rally in bitcoin, the Friday anomaly appears to be back. Our best guess continues to be that the phenomenon has to do with a combination of fund flows and money moving onto retail exchanges ahead of the fiat banking system closure over the weekend. The Friday phenomenon does appear to be positively correlated with bitcoin’s price, lending credence to both of those theories.

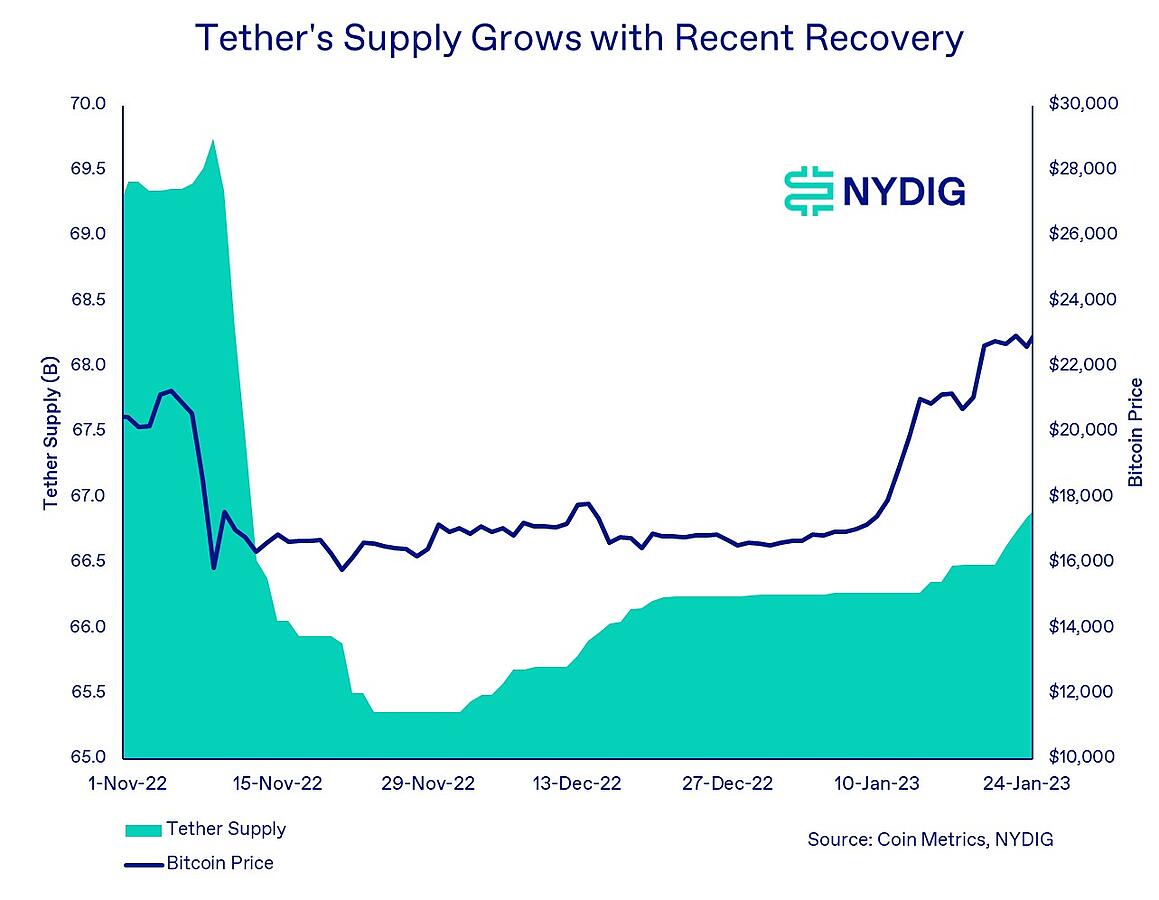

Tether Supply Ramps While Binance USD Shrinks

The supply of the Tether (USDT) stablecoin continues to grow amidst the bitcoin price rally as new capital comes into the digital asset ecosystem. Despite share losses to other stablecoins, Tether continues to be the most important stablecoin for exchange trading with $984B of transaction volume over the past 30 days compared to Binance USD (BUSD) at $323B and USD Coin (USDC) at $135B, according to CoinMarketCap. Tether trading even surpassed bitcoin, which traded $958B over the past 30 days.

We think the continued growth of Tether supply is a positive indicator for the continued price rally. For those without the context of the 2019 recovery, growing Tether supply was an important indicator during its rally from the cycle lows set in December 2018 to the mid-year highs. During this rally, the price of bitcoin went from $3,250 to just over $13,000 before falling again in the second half of the year. We encourage investors to watch the supply of Tether as an indication of capital coming into the digital asset ecosystem. USDT is an important quote currency for trading pairs on many crypto exchanges, especially those that do not accept cash deposits.

However, the same trend cannot be said for the second and third largest stablecoins, USDC and BUSD. USDC supply has been chopping around the 42B – 44B range while BUSD supply has been declining. The decline in BUSD comes amidst investor concerns on several fronts including general fears that emerged about the reserve status of the Binance exchange following a proof of reserves report from Mazars which was removed from the company’s website, concerns about practices around the issuance of BUSD on blockchains other than Ethereum that may have resulted in unbacked BUSD being created, and the report of comingling of BUSD deposits with other exchange client assets. BUSD is a multichain asset with the chief asset issued on the Ethereum blockchain by Paxos and regulated by the New York State Department of Financial Services. Binance then takes these Ethereum BUSD assets, self-custodies them, and issues BUSD tokens on the BNB Chain, Avalanche, Polygon, and TRON, in a process called “wrapping”, something it has done for 94 tokens. While we would be surprised if these assets were not sufficiently backed, Binance should seek to provide better clarity and disclosures around the process and collateral for these wrapped assets.

No Evidence Binance Trading is Leading the Rally

The price of bitcoin is up nearly 40% year to date, leaving some traders positioned for more downside scratching their heads. We have explored a number of factors at play during the rally, but many in the crypto community are pointing to trading action on Binance as the reason for the rally. However, an analysis of the data show no discernible premium for bitcoin traded on Binance over Coinbase. If traders on Binance were driving the rally, we would expect to see some premium compared to other exchanges like Coinbase. The average rolling 12h premium during this recent rally for Binance over Coinbase was just 0.01% over the past month.

Market Update

Bitcoin’s winning streak continued this week with the price rising 9.5%. This brings the year-to-date return to 39.6%, making this January so far one of the best monthly returns on record. In January 2011 and 2013, bitcoin was up 73.3% and 54.5% respectively. Coincidentally, both of those years were stellar years for bitcoin returns. Equities also had a strong week with the S&P 500 up 3.0% and Nasdaq Composite up 6.1%. Commodities were up with gold up 0.3% and oil up 1.0%. Bonds were mixed on the week with investment grade corporate bonds down 0.3%, high yield corporate bonds up 0.5%, and long-term US Treasuries down 0.9%.

Important News This Week

Companies:

Amazon NFT Initiative Coming Soon - Blockworks

Silvergate Suspends Series A Preferred Stock Dividend - Silvergate

Wilshire Announces Partnership with FalconX as its Preferred Digital Asset Index Product Provider - Wilshire

Investing:

Binance Admits Past Management Issues With BUSD-Peg Stablecoin Reserves - Bloomberg

Roger Ver Says He Won't Pay Genesis $20M For Bad Trades - Blockworks

Regulation and Taxation:

The Administration’s Roadmap to Mitigate Cryptocurrencies’ Risks - White House

Binance Moved $346M for Seized Crypto Exchange Bitzlato, Data Show - Reuters

Top US Securities Regulator Quashed Circle’s Efforts to List Through SPAC - FT

U.S. Securities Regulator Probes Investment Advisers Over Crypto Custody - Reuters

Federal Reserve Board Announces Denial of Application by Custodia Bank, Inc. to Become a Member of the Federal Reserve System - Federal Reserve Board

Federal Reserve Board Issues Policy Statement to Promote A Level Playing Field For All Banks With A Federal Supervisor, Regardless Of Deposit Insurance Status - Federal Reserve Board

Upcoming Events

Feb 1 - FOMC rate decision

Feb 14 - January CPI reading