IN TODAY'S ISSUE:

- Bitcoin rose 47.2% during the quarter, delivering on Q4 seasonality and besting every asset class by a wide margin. The US elections, in which crypto played a significant role, were the main driver to pushing bitcoin through $100K.

- Bitcoin also rose 119.6% in 2024, notching its second consecutive triple-digit percentage annual gain. Bitcoin continues to outpace every asset class, even as the S&P 500 registered back-to-back +25% gains.

- Bitcoin ETFs registered $16.5B of net inflows, but the lion’s share of flows is going to BlackRock and Fidelity while some ETFs registered outflows during the quarter.

- Futures-based ETFs such as the ProShares Bitcoin ETF (BITO) remain relevant despite underperforming the spot ETFs by 10.87% (total return) in 2024 (since the launch of spot ETFs).

- Corporate investment in bitcoin was a big story in Q4, driven by MicroStrategy. Ironically, most of MSTR’s outperformance vs BTC has come since the spot ETFs launched.

- The Trump administration continues to come into view post-election; however, we would caution on expecting immediate changes. Key officials still need to be named, those that have been named need to go through the confirmation process, and then once confirmed they need to assemble their staff.

- The US bitcoin strategic reserve is a highly topical item, but how it comes to be (law vs Executive Order) and its implementation (acquisition vs using existing seized coins) matter greatly as a catalyst.

- ETFs are hitting their one-year mark, and, despite their unbelievable success, they need this type of “seasoning” before major banks and wealth platforms integrate them into their advisor platforms.

- FTX creditors are set to receive $16B in cash by early March, which could be an important catalyst for the market in Q1.

- Bitcoin “L2s” will likely be highly topical going forward as investors continue to demonstrate the desire to put “bitcoin capital” to work despite a myriad of technical, legal, and regulatory risks.

PERFORMANCE REVIEW

Bitcoin Beats Every Other Asset Class Fueled by the US Elections

Bitcoin scorched to new highs this quarter driven by the US election outcome in which pro-Bitcoin candidate Donald Trump took the White House and Republicans took the Senate and retained control of the House. Given the outcome of the election, one in which crypto played a prominent role, it comes as no surprise that bitcoin bested every other class during the quarter. But even before the election, bitcoin was already having a pretty good quarter, up over 12%. However, it was the election outcome that turbocharged returns, sending bitcoin up 47.2% for Q4.

While there was a bit of sector and style rotation in the days following the election, much of that was short-lived – for example, small cap value stocks got some (temporary) attention, but the small cap value trade had completely roundtripped by year-end. Much of what worked in the quarter were sectors and styles that could’ve been predicted by a Republican sweep – outperformance for the US dollar (US protectionism) and financials (lower regulation) and underperformance of the healthcare sector (Republican opposition) – or were just continuation of trends that been present for many years now – outperformance by large cap, growth, tech and consumer discretionary stocks. The “Trump trade” in 2016 was very different – the election outcome was a much bigger surprise initially and the sector and style rotation lasted well into 2017.

Bitcoin Outperforms Every Asset Class by a Wide Margin in 2024

Bitcoin rose 119.6% in 2024, outperforming every other major asset class by a wide margin. Moreover, this is the second consecutive year of outperformance for bitcoin which comes during a period of very strong returns for most asset classes, including US equities. Bitcoin rose 119.6% in 2024 versus the S&P 500 at 25.0% and Nasdaq Composite at 29.6%; Bitcoin rose 156.9% in 2023 versus the S&P 500 at 26.3% and Nasdaq Composite at 44.7%. US equities have been white hot the past 2 years, but their returns still have not been able to match bitcoin’s.

Ranking Bitcoin’s Returns

The fourth quarter is usually a seasonally strong period for bitcoin returns and this year was no different. While bitcoin’s 47.2% return was impressive, it ranked only 6th best in terms of Q4 performance going back to 2011. Still, this was well above the median Q4 return of 10.5% (average returns are skewed by some very high years).

Bitcoin’s 119.6% return in 2024 put it 8th best on the annual ranking list, pretty much middle of the pack. As the penultimate year in bitcoin’s repeating 4-year cycles (2012, 2016, 2020), its annual return was lower than the previous 3 (189.1%, 124.3%, 308.5%), but this is something to be expected as bitcoin grows larger – it will be difficult to compound at similar rates.

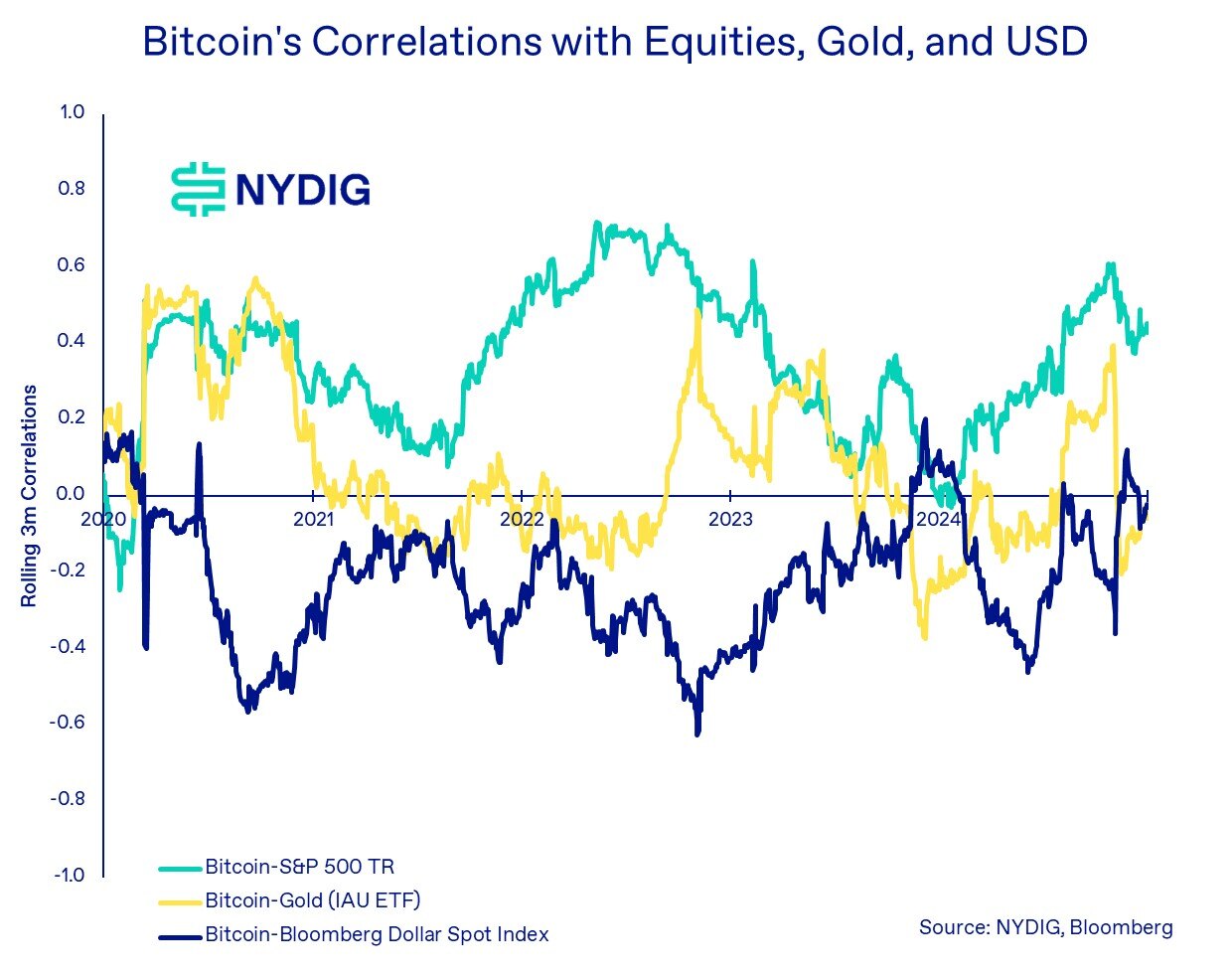

Correlations Come in Following the Election

Bitcoin’s correlations with major asset classes, US equities, gold, and the US dollar index, fell (absolute levels) during the quarter, much of it on the back of the election. Bitcoin’s correlations with US equities pulled back from levels not seen since the 2023 “correlation crisis.” With bitcoin increasingly owned by traditional market investors, it’s natural to expect correlations to change. Still, the promise of a non-sovereign issued store of value is an appealing investment in the current geopolitical climate, one that should not be driven by the same macroeconomic levers of say the US stock market.

THE EVENTS THAT SHAPED THE QUARTER

US Election the Highlight of the Quarter

The US election, in which Republicans gained or maintained control of the White House, Senate, and House, unquestionably stood out as the highlight of the quarter. Not only is President-Elect Donald Trump explicitly pro Bitcoin, but many elected officials who were in opposition to crypto broadly were ousted. Credit that to the effect PACs and their spending broadly had on election outcomes.

While the election was a decisive point in time during the quarter, what has followed in the days since the election has been an assembling of cabinet members, agency heads, and advisors. Not all of Trump’s picks have been revealed yet, but from what we know so far for the agencies that matter (Treasury, SEC, Commerce, White House advisors) regarding crypto and Bitcoin, we like what we see. We still do not know who might run critical agencies, such as the CFTC, OCC, and FDIC, but we expect that they will be pro Bitcoin and crypto as well. The recent release of FOIA’d letters between banking regulators and banks has given an eye-opening look into how the Biden administration impeded the industry’s growth last cycle. We expect a very different tone going forward.

ETFs Score Big Inflows, but Not All Funds Benefitted Equally

The spot bitcoin ETFs were big winners during the quarter, gathering $16.5B of net inflows during the quarter. However, the bounty was hardly split evenly between the industry participants. Of the $16.5B of net inflows, $15.8B went to BlackRock and $1.9B went to Fidelity while Grayscale lost $1.0B (across GBTC and BTC). Outside of these firms, there was little to go around to the other funds. VanEck took in $141M. 21Shares lost $264M. Little else was of note with the industry players, which may be important commentary - investors have consolidated around a few big winners.

Other items of interest across the ETF landscape include renewed flows into levered long funds while investor appetite for single leverage futures funds remains subdued. The fact that single leveraged futures-based ETFs like the ProShares Bitcoin ETF (BITO) remain relevant is surprising to us given the fee differential, futures roll cost, and tracking error to spot. In 2024 since the start of spot trading, the total return of BITO underperformed the spot ETFs (using IBIT as the proxy) by 10.87% (BITO +90.22% vs IBIT 101.09%). This is an enormous cost to investors.

Canadian ETFs showed significant outflows during the quarter, highlighting the geographic difference between US and Canadian investors. The big catalyst this quarter was in the US, not Canada. Aside from big initial seed investments, the Hong Kong ETFs have shaped up to be underwhelming and Q4 was no exception. It is unlikely these become big demand drivers unless something changes structurally, like access to them for mainland investors.

MicroStrategy and Corporates Go Big

MicroStrategy, which has been on the vanguard of corporate investment in bitcoin, went even bigger in Q4, announcing a $42B strategy to acquire even more. Initially targeted at a 50/50 split of equity and debt with $10B earmarked for 2025, the company somehow one-upped that, adding on $2B of preferred stock and issuing $14.2B in shares alone in Q4. To say the company is running ahead of its initial plan would be an understatement. We would not be surprised to see the company issue more stock as it seeks to increase the number of shares it has authorized at a January 21 shareholder meeting.

But it was not just MicroStrategy that purchased bitcoin for its balance sheet. Seventy public companies now own nearly $56B worth of bitcoin (MSTR owns $42.1B of that), including MercadoLibre, NEXON, Genius Group, Semler Scientific, and Metaplanet. This second wave of corporate adoption, the first of which occurred in 2021 with companies such as Tesla and Block (Square), seems to be gathering steam rather than fizzling.

The odd thing about the MicroStrategy part of corporate adoption is that while its stock price outperformed bitcoin in the 2021 bull market, it was not until after the bitcoin ETFs launched that its stock price started to really outperform bitcoin. One might have expected the appearance of spot ETFs that allowed investors to invest at NAV to reduce the interest in a vehicle like MSTR. Instead, it seems to have done just the opposite of that, it turbocharged it.

ETF Options Begin Trading

Options on the bitcoin ETFs began trading on 11/19 with IBIT, followed the next day by a host of others. Either because of the one-day head start or the prominence of the IBIT ETFs versus every other spot bitcoin ETF, the competition for options trading on the ETFs was not even close, with IBIT options the clear volume leader. ETF options are important market development allowing investors to engage in hedging strategies, express directionality with leverage, and for banks to create structured products. Structured products could be a big driver in 2025, one that results in demand for the underlying bitcoin and supply of volatility, suppressing its volatility. Ironically, these could work in a self-perpetuating cycle where declining volatility makes structured products more attractive in risk parity strategies, which then results in more demand for underlying bitcoin and further volatility suppression.

LOOKING AHEAD

Administration, Key Objectives Come into View

Inauguration Day is 10 short days away, ushering with it the renewed hope for the new administration to execute many of its campaign promises. Many can happen quickly, but some may take some time. The execution of these initiatives may be a matter of priority, with items like geopolitical conflict, the budget and debt ceiling, global trade and tariffs, and immigration perhaps more pressing matters.

The US strategic bitcoin reserve could come quickly via an Executive Order, one of which has already been written by a Bitcoin advocacy group and circulated on social media. However, that avenue would be much less permanent, one that could be revoked by the next president. Legislation, like the BITCOIN Act introduced by Senator Lummis, would be a more permanent solution but must be approved by Congress, and thus likely to take more time.

Regarding cabinet members and agency heads, Gensler is already out at the SEC but his likely replacement, Paul Atkins, still needs to be confirmed and sworn into office. Gensler wasn’t sworn into office until April 17th, 2021, to give readers a sense of timing. Heads of the CFTC, OCC, and FDIC have yet to be named. It will be at least several months before these nominees have hearings, get confirmed, and start working and assembling their top staff.

With the US strategic bitcoin reserve, form (EO vs bill) and function (methodology) matter greatly for the market. If the bitcoins come from confiscated funds the government already controls (198.1K BTCs worth $18.3B), that alleviates an overhang that the US would be a seller of bitcoins, but it doesn’t create incremental demand. Complicating matters, 119,754 of the bitcoins in the US government’s possession came from Bitfinex, sister company of Tether, which has strong ties to the current administration. We don’t know how that conflict would be resolved, but it’s hard to imagine Bitfinex willingly parting with $11.0B.

Other important crypto legislation, like FIT 21 and the stablecoin legislation, may take some time to pass. A reinvigorated conservative and free market legislature may be less willing to compromise on points than when liberals controlled the Senate. Other Trump promises, such as “made in the USA bitcoin,” while a nice overture to the mining industry, gives us little to analyze, leaving much up to speculation.

Final and Best Year of the Four-Year Cycle

If patterns repeat, 2025 will be the fourth year in bitcoin's repeating price cycle. There’s a lot of reason to believe that this year will be good for bitcoin, too (see this section). While the market prognosticators disagree as to how high bitcoin might eventually go or if the cycles ultimately are broken for sustained long-term secular growth, predictions are all without exception higher than current prices (including ours). This says something about investor attitudes towards the market and while we aren’t ones to be contrarian without good reason, positioning is an important aspect of active management.

FTX Creditors to Receive $16B in Cash

Creditors in the FTX bankruptcy plan are set to receive $16B in cash by early March. The bankruptcy plan became effective January 3rd, and the organization has agreed to repay creditors within 60 days, by March 4th. This is an important catalyst as the claims largely stem from FTX trading clients who may be eager to convert their cash disbursements (creditor payments are being made in cash, not in-kind or crypto) back into crypto. Some portion of claims may have traded hands to investment firms specializing in bankruptcy claims, which would be less likely to be used to repurchase crypto.

Putting Idle Capital to Work

Much technological development in the Bitcoin ecosystem over the past 6 - 12 months has been around making the bitcoin asset more productive, typically by bridging, wrapping, or locking up bitcoin, and issuing another asset on a 1-for-1 basis on another network or sidechain. While some in the community like to call these “layer 2s,” that’s a generous description in our eyes. A full critique of the myriad of “L2” options is out of the scope of this piece, but we have noticed a strong desire on behalf of investors to put bitcoin’s idle capital to work – as the stake helping to secure Proof of Stake (PoS) networks or as an asset in DeFi providing liquidity, being lent out, or as the collateral for on-chain collateralized stablecoins. We think this could be a big and continuing trend in the coming quarters. Of course, caveat emptor with the specific implementations that enable this as they can entail legal, regulatory, or technical risks, or likely all three.

ETFs Season as Wealth Platforms are the Big Opportunity

Most investors tend to think about bitcoin’s supply when thinking about its investment case; we tend to think about the flip side, demand (yes, its fixed supply is an important feature). With each cycle, there’s been a new investor class or geography driving demand. With the spot bitcoin ETFs being the new feature this cycle, there’s still a big opportunity to unlock, the wealth and advisory at the major banks, which control trillions in assets.

Typically, new products like these ETFs need a period of operational and return history before being greenlit for advisors. The spot bitcoin ETFs are on the threshold of having their first year under their belt, which may qualify as the minimum amount of time needed for these platforms to seriously consider these products. We know of no concrete imminent plans for banks to proactively offer bitcoin ETFs to their clients, but it’s something we’re on the lookout for.

Banks Custody Crypto

BNY’s exemption from SAB 121 reporting requirements was highly topical in Q4 and we would expect other bank custodians to seek similar exemptions or have SAB 121 dropped entirely. While some of these custodians may go after the bitcoin and ether ETF opportunity, we think a more likely use case is the custody of real-world assets (RWAs), like money market and government bond funds as well as other types of traditional financial products, but on the blockchain.