IN TODAY'S ISSUE:

- We look at what the options market says about trader positioning ahead of some key ETF dates.

- The overhang continues, with payouts delayed a year in the Mt Gox bankruptcy case.

- Fed Rate policy hits stocks and bonds, but bitcoin ends the week flat.

Forward Volatility Highlights Trader Positioning Around Key ETF Dates

A jump in volatility in the options market indicates that traders are expecting a significant movement in spot prices around key ETF dates. The forward volatility of at-the-money (ATM) options in the middle of October, the window in which the SEC needs to respond to the BlackRock iShares Bitcoin Trust ETF, shows a significant increase. Forward volatility jumps 9.6 points from 10/13/23 to 10/20/23, indicating the market expects a 5.5% single day move, either up or down, in the underlying spot price of bitcoin, during that window.

As a reminder, the SEC has up until October 17th to respond (approve, deny, or delay) to the Nasdaq’s request to list the iShares bitcoin fund (see tables below for all key dates). Technically, the SEC can respond at any time before that date, but historically these decisions are left until a few days before the deadline. The SEC also has until October 16th to respond to the Bitwise Bitcoin ETP Trust, one day before the BlackRock ETF. The options market indicates that traders are expecting price volatility around that period, which could be because of an approval or denial. There is one more important date for investors to key on, October 13th. This is the final date for the SEC to appeal the decision in the Grayscale case, which could give clues to how the agency is thinking about its posture around spot ETFs.

Halloween Trick: Mt Gox Pushes Deadline to 2024

This week, the trustee overseeing the Mt Gox bankruptcy made the decision to delay creditor payouts for an additional year. Initially set for October 31st, 2023, the new payout date is now October 31st, 2024. The resolution of this infamous incident in crypto history has been a prolonged process, spanning over 9 years and involving approximately 138K BTC, which is equivalent to about $3.7B at current prices. The disbursement of funds and the satisfaction of creditor claims have been widely discussed within the industry, particularly due to its impact on market prices. With the approaching Halloween deadline this year, we had hoped to finally close this chapter and move forward, despite any potential market volatility. Unfortunately, it seems that the persistent overhang will continue to linger for another year, although some begin as early as the end of this year. Although we can temporarily set aside thoughts of fund disbursement, we will regrettably have to revisit this topic again next year instead of progressing forward.

Fed Rate Policy Crimps Risk Assets

In a highly anticipated move this week, the FOMC made the decision to keep interest rates unchanged. However, their indication that another rate hike could potentially occur before the end of the year sent ripples through the market, causing a decline in assets prices, including stocks and bonds. Bitcoin initially sunk on the news as well, but ended the week unchanged, something that cannot be said for stocks and bonds.

Over the year, there has been much speculation about the correlation between macroeconomic factors and the price of bitcoin. Factors such as the value of the US dollar, inflation readings, inflation expectations, real yields, nominal yields, forward rate expectations, and monetary aggregates have all been suggested as potential causes for bitcoin's movement. However, the reality is that none of these factors fully explain the price fluctuations of bitcoin over the past decade. However, when we shift our focus to shorter time frames, such as 5-, 3-, and 1-year horizons, factors such as inflation expectations and real yields start to play a more significant role. Nevertheless, we still believe that the unique and idiosyncratic features of bitcoin itself are the primary drivers of its price.

Although certain macro factors may appear more influential during specific time periods, such as the rising rate expectations starting in November 2021, it remains challenging, if not impossible, to identify factors that consistently explain bitcoin's price history. Macro factors seem to come in and out of favor with explaining bitcoin returns.

Market Update

Despite experiencing some fluctuations during the week, the price of bitcoin remained relatively flat. As previously mentioned, various asset classes encountered challenges due to the uncertainty surrounding potential interest rate hikes. Equities saw a steep decline, with the S&P 500 dropping by 2.3%, and the Nasdaq Composite experiencing a 5.0% decrease. In the fixed income market, investment grade corporate bonds fell by 1.3%, high yield bonds by 1.4%, and long term US Treasuries by 3.0%. Interestingly, gold managed to hold price, showing a slight increase of 0.4%, even as real yields surged. On the other hand, oil experienced a 0.6% decrease after a significant rally over the past month.

Important News This Week

Investing:

Mt Gox: Notice Concerning Change of Repayment Deadlines - Mt Gox Rehabilitation Trustee

Grayscale Investments Files for New Ether Futures ETF - The Block

Regulation and Taxation:

DFS Announces Updates to Virtual Currency Oversight - NYDFS

How the Lazarus Group is Stepping Up Crypto Hacks and Changing its Tactics - Elliptic

U.S. SEC’s Crypto Enforcement Chief Warns Charges Won't End at Coinbase, Binance - CoinDesk

Companies:

Citi Develops New Digital Asset Capabilities for Institutional Clients - Citi

Bringing Capital Markets On-Chain with DTCC and Chainlink - DTCC

Tether Is Lending Its Stablecoins Again - WSJ

AI’s New Backer: Stablecoin Tether Makes A $420 Million Bet on Cloud GPUs - Forbes

PayPal USD Is Now Available on Venmo - PayPal

PayPal USD August Holdings Report - Paxos

Upcoming Events

Sept 29 - CME expiry

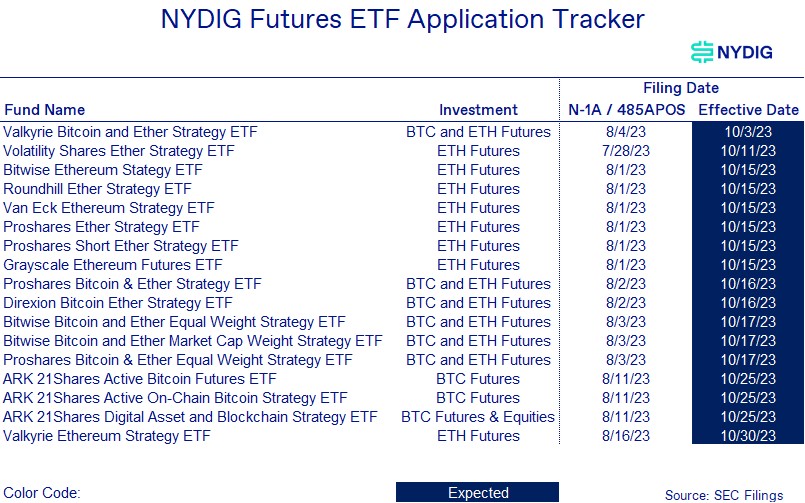

Oct 3 - Valkyrie Bitcoin and Ether Strategy ETF effective date

Oct 13 - SEC appeal deadline in Grayscale case

Oct 16 - Next SEC response date for first (Bitwise) of the spot bitcoin ETF