IN TODAY'S ISSUE:

- The implications of Visa's stablecoin strategy expansion for payments.

- Stablecoins have emerged as one of the blockchain killer applications, with stablecoin transactional volumes approaching that of Mastercard.

- Industry focuses on infrastructure and building transactional supply, but increasing transactional demand is also necessary.

Visa News Highlights the Importance and Utility of Stablecoins

Visa caused a stir last week with its announcement of settling merchant payments using the USD Coin (USDC) stablecoin on the Solana blockchain, in collaboration with merchant acquirers Worldpay and Nuvei. This exciting development builds upon Visa's ongoing efforts in the realm of digital currency, granting them the capability to settle payments with issuer and acquirer partners using the USDC stablecoin, albeit in the pilot stages. While Visa had previously relied on USDC issued on the Ethereum network, they have now expanded their capabilities to include USDC issued on Solana.

The Size and Style of Stablecoins

Undoubtedly, stablecoins, digital assets that closely mirror the value of the US dollar (USD), have emerged as one of the most important applications of blockchain technology. The collective value of stablecoins currently stands at a staggering $124.4 billion, with the majority being in the form of off-chain reserve style assets like Tether (USDT) and USDC. Additionally, there is a smaller portion of over collateralized on-chain reserve style stablecoins such as Dai (DAI), as well as a fraction of undercollateralized algorithmic stablecoins like Frax (FRAX). Despite its controversial history, Tether still dominates the stablecoin market, accounting for approximately two-thirds of the industry's total value.

At first blush, a centrally issued USD proxy might seem antithetical to the ethos behind the creation of the first digital asset, Bitcoin, a fixed supply asset which was created to eliminate the reliance on financial intermediaries. Most stablecoins (off-chain reserve style), rely on a central issuer and because they mimic the USD, inheriting the same economic, social, and governance characteristics of the USD. While many stablecoins have started off as a single asset on a single network (Omni/Bitcoin for USDT, Ethereum for USDC), today most “stablecoins” are a collection of unique digital assets across many networks, 13 in the case of USDC and 15 in the case of USDT.

Stablecoin Volumes Catching up to Mastercard

However, despite these facts, stablecoins have not been deterred from gaining immense popularity. This is a clear indication of the growing demand for "USD on a blockchain," whether it be as a reliable store of value, a convenient medium of exchange, or even as a quoted currency in the trading of various assets (such as BTCUSDT). In fact, stablecoins have become so widely embraced that their combined transactional volume now surpasses that of Bitcoin and is on the verge of surpassing even Mastercard, the second largest card network. While we acknowledge that this is not necessarily an apples-to-apples comparison, it still provides valuable insight. It's important to note that the volumes of credit card networks primarily consist of payments, whereas stablecoins and Bitcoin can be used for a range of financial applications, including payments, although the exact proportion is difficult to determine.

The Industry's Focus on Transactional Supply

When taking a step back and looking at the bigger picture of the crypto industry's technological advancements, it becomes evident that much of the focus lies in expanding the availability of transactions for users. Various layer two technologies, such as rollups, app chains, sharding, and side chains, along with faster layer one blockchains like Solana and the Lightning Network, are all pioneering innovative ways to make crypto faster and more cost-efficient. Visa's support of USDC on Solana is particularly noteworthy because, despite the occasional blockchain outages, Solana was created to deliver high-speed and low-cost transactions all on a single chain. However, it begs the question: should the industry place equal emphasis on transactional demand as it does on transactional supply? For those building companies in the industry, a fruitful strategy might involve focusing on the functions that are not adequately provided by the existing technology. The Bitcoin protocol inherently provides many of the functions that users desire, as it was designed to eliminate intermediaries. This inherently makes building enduring companies in the industry a challenge.

Crypto has the potential to follow in the footsteps of the internet, where faster speeds and widespread accessibility opened up new and previously unimaginable possibilities. Just like how we could envision watching TV over the internet during the dial-up era, but never could have imagined services like Uber, Twitch, or the widespread influence of social media. It is these unexpected opportunities that make the future truly exciting.

Market Update

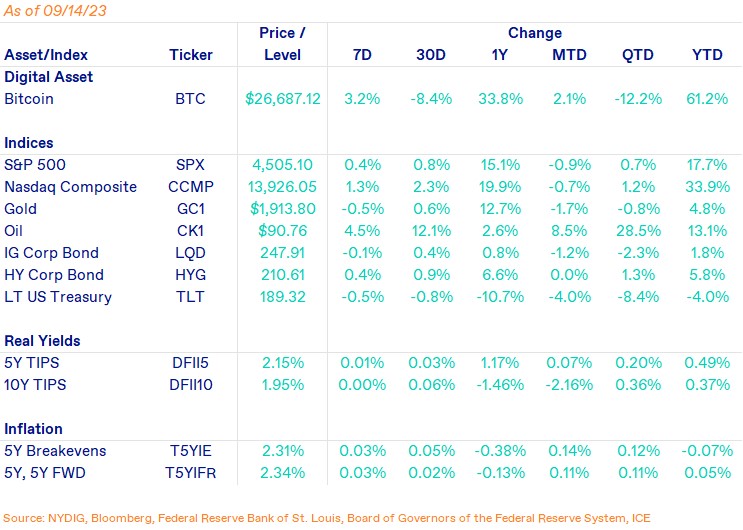

Despite experiencing some fluctuations during the middle of the week, bitcoin managed to conclude the week on a positive note, with a 3.2% increase. The price of bitcoin dropped to as low as $24,900 on Monday due to news of FTX's decision to liquidate its digital asset holdings in order to meet the demands of its creditors in the bankruptcy case. FTX currently possesses $560 million worth of bitcoin within its $3.4 billion digital asset portfolio. However, the sale process only permits a maximum of $50 million in digital asset sales during the first week, followed by $100 million per week thereafter, with court permission. Ultimately, FTX may be allowed to sell up to $200 million worth of digital assets per week, again with the court's approval. Equities experienced a rebound this week, with the S&P 500 rising by 0.4% and the Nasdaq Composite increasing by 1.3%. Additionally, the price of oil continued to rise steadily as suppliers tightened their output. Conversely, gold witnessed a slight decline of 0.5% as real yields remained stable.

Important News This Week

Investing:

Hedge Fund Brevan Howard Sees Outsized Returns from Digital Assets - Bloomberg

An Important Shift in Fed Officials’ Rate Stance Is Under Way - WSJ

FTX Can Begin Selling Its Digital Assets, Bankruptcy Court Rules - Blockworks

Genesis No Longer Offering Trading Services Through Any Business Units - The Block

Regulation and Taxation:

SEC Charges Creator of Stoner Cats Web Series for Unregistered Offering of NFTs - SEC

Brian P. Brooks—former Acting US Comptroller of the Currency—Rejoins O’Melveny - O'Melveny

Sherrod Brown Letter Regarding Crypto Disclosure to Treasury, SEC, and CFTC - US Senate

Companies:

PayPal Partner Paxos Overpaid $510,750 In the Largest USD Bitcoin Transaction Fee Ever - Bitcoin Magazine

Paxos 'Fat Finger' Overpayment Is Returned by Bitcoin Miner F2Pool - CoinDesk

Lightspark CEO David Marcus on Trying to Turn Bitcoin into a Global Payment Network - CNBC

Binance US CEO Brian Shroder Departs as Company Lays Off One Third of Its Staff - Bloomberg

JPMorgan Looks to Save Millions With Blockchain-Based Financial Instruments - Blockworks

Banking Powerhouse HSBC Working with Crypto Custody Firm Fireblocks: Sources - CoinDesk

Swift Says Three Central Banks Are Testing Its CBDC Interoperability Solution - The Block

Bitcoin Electricity Consumption: An Improved Assessment - Cambridge Judge Business School

Upcoming Events

Sept 22 - FOMC interest rate decision

Sept 29 - CME expiry

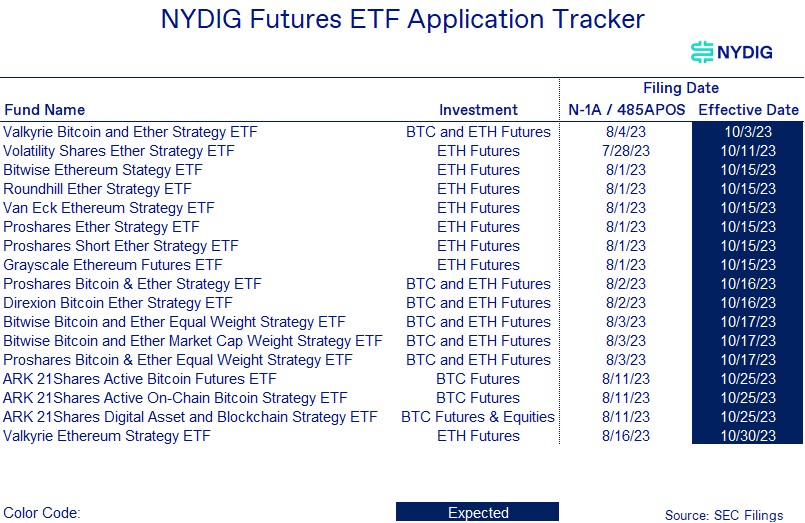

Oct 3 - Valkyrie Bitcoin and Ether Strategy ETF effective date

Oct 13 - SEC appeal deadline in Grayscale case

Oct 16 - Next SEC response date for first (Bitwise) of the spot bitcoin ETFs

Oct 31 - Mt Gox claims payment date