IN TODAY'S ISSUE:

- A trading metric for bitcoin ETFs yields valuable insights into owners of ETFs.

- Strange trading data create outliers of two ETFs.

- The similarities of the launch of bitcoin ETFs with the launch of GLD in 2004.

What Trading Data Says About ETF Holders

Since the introduction of spot bitcoin ETF trading in the US, there has been a prevalent question circulating - "who are the owners of these ETFs?" With a plethora of bitcoin ownership options already accessible to investors, ranging from private bitcoin funds to self-custody to third-party spot custodial services, the important question was about the attraction of investing in bitcoin through an ETF structure. Although we have some answers already (hint: they’ve been very popular), concrete answers have remained somewhat elusive, and we believe a deep dive into ETF trading data can unveil valuable insights into the ownership of these funds.

At the core of our analysis lies the turnover ratio, a metric derived by dividing the dollar trading volume by the total net asset value (NAV) of the fund. This ratio shows the proportion of the fund's assets traded on any given day, offering a glimpse into the investor and trader profiles and potentially what motivates their investment choices. Notably, even within same asset class, like the S&P 500, ETF families (such as iShares, SPDR, Vanguard, etc.) showcase significantly different turnover ratios. This implies that the turnover ratio is not a blanket indicator for the entire asset class but rather sheds light on distinctive characteristics of individual ETFs.

Spot ETF Comparisons

We analyzed the turnover ratios of individual funds (5-day trailing average) along with an aggregate measure of all spot bitcoin ETFs (also on a 5-day trailing average). The intention behind the latter was to gain insight into the entire spot bitcoin ETF landscape, especially considering the multitude of simultaneous launches. It is rare occurrence to witness such a competitive scenario amongst various players simultaneously entering the market in an asset class, the only such instance we are aware of. The collective turnover ratio of bitcoin ETFs is significantly influenced by Grayscale Bitcoin Trust (GBTC), which today holds the majority share of ETF assets (~60%).

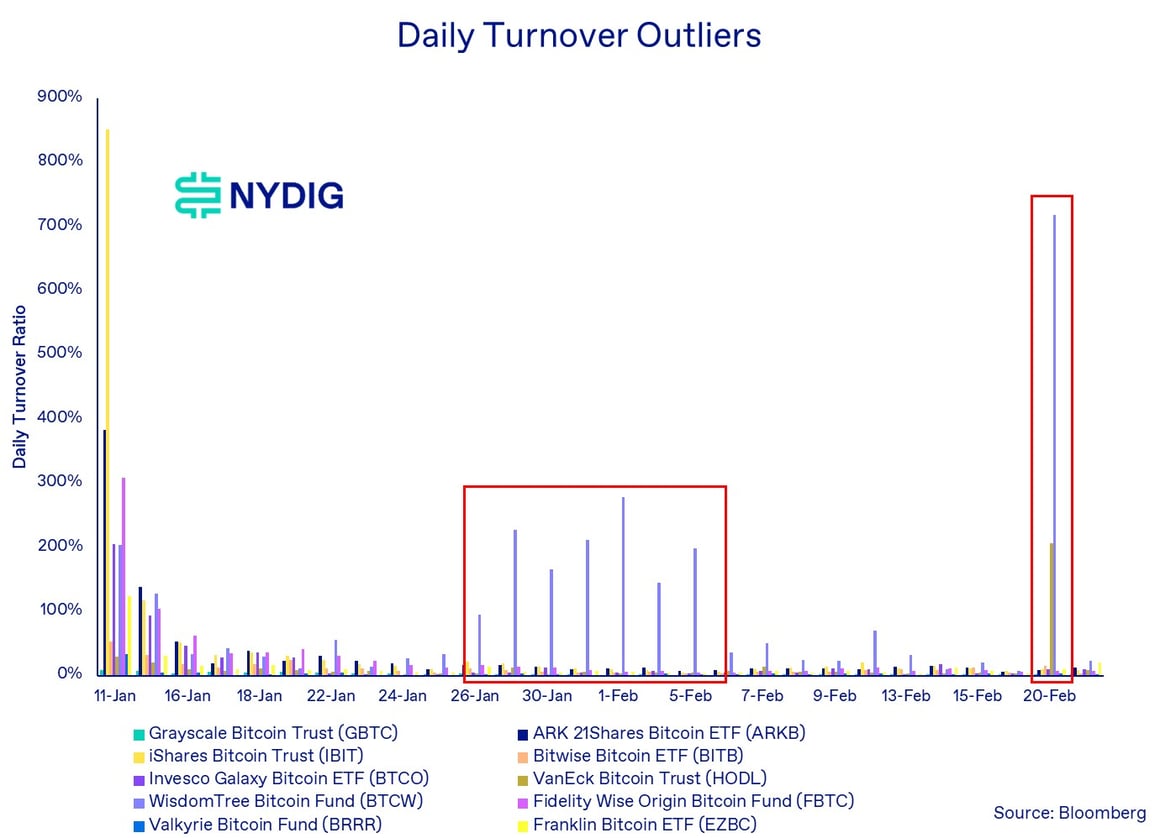

Following the initial buzz of trading activity during launch, which may have seemed misleading due to minimal inflows in the early days, the trend has now stabilized to more consistent levels. At the lower end of the turnover spectrum, we have Valkyrie Bitcoin Fund (BRRR) at 2.2% and Grayscale Bitcoin Trust (GBTC) at 2.4%. On the higher end of the "normal" range sits ARK 21Shares at 11.3%, with the overall spot bitcoin ETF complex at 5.3%. There are two funds that stand out as outliers due to their unusual trading patterns, WisdomTree Bitcoin Fund (BTCW) and VanEck Bitcoin Trust (HODL), but we'll delve deeper into that in the upcoming section (please note the different axis for BTCW in the chart to follow).

WisdomTree and VanEck are Outliers

There are two ETFs that stand out in terms of turnover ratio compared to the typical spot ETFs: the WisdomTree Bitcoin Fund (BTCW) and the VanEck Bitcoin Trust (HODL). HODL's turnover ratio remained consistent with other ETFs until Tuesday (2/20), when its trading volume experienced a significant spike, reaching nearly $400M for the day. The cause of this behavior remains unclear. We have previously emphasized that daily trading volume is not a reliable indicator of daily fund flows, a misconception prevalent in the industry and particularly highlighted in this instance. The inflows were only $5.9M for the day. The substantial increase in trading on 2/20, a 54x surge compared to the trailing 5-day average for daily turnover, is indeed puzzling.

On the other hand, BTCW has consistently been an outlier. It also saw a remarkable surge in volume on 2/20, 35x the trailing 5-day average for daily turnover. But it has maintained a turnover ratio well above that of every other ETF. With the smallest net asset value among spot ETFs at $35.7M compared to the next largest fund, Franklin Bitcoin ETF (EZBC), at $100.6M, BTCW commands less than 0.1% of the collective net assets value of spot bitcoin ETFs. However, its trading activity, relative to its size, is extraordinary, with a peak 5-day average turnover ratio of 205%. Even at the low of 27.8%, BTCW's turnover ratio surpasses that of the next highest ETF by over 2.5 times since trading stabilized post-launch. We welcome any theories on why these outliers persist but are currently at a loss to provide a definitive explanation, other than attributing it to potential excessive trading.

Equity Comparisons Highlight Differences in ETF Families

We compared the aggregate bitcoin ETF turnover ratio to that of other asset classes: a broad measure of equities, the S&P 500, and to tech stocks, which might share some similarities to bitcoin. Our findings revealed that the turnover ratio for aggregate bitcoin ETFs is lower than the leading funds in their respective sectors, such as SPY for the S&P 500 and QQQ for tech stocks, yet higher than the lesser-known funds within these asset classes. When considering the aggregate of S&P 500 ETFs, similar to our approach with spot bitcoin ETFs, the turnover ratio would be lower than that of bitcoin ETFs as SPY lacks a significant net asset value weighting advantage over IVV and VOO. On the other hand, QQQ possesses a substantial net asset value advantage over XLK and VGT, presenting a potentially different scenario in that regard.

Options Markets Likely the Differentiating Factor for Turnover Ratio

We think that the primary distinguishing factor affecting turnover ratios for S&P 500 ETFs and tech stock ETFs (the underlying indexes are different) is options markets. SPY and QQQ have some of the most liquid and active options markets and demand for delta hedging by dealers is likely the reason for the turnover ratio disparities. Dealers are hedging their delta exposure on the options they sell (dealers are typically net short options contracts) by trading in the underlying markets, SPY and QQQ. This gives rise to the turnover ratio disparities. By comparison, IVV and VOO, as well as XLK and VGT, have less robust options markets and therefore there is less demand for to trade the underlying shares.

Bitcoin ETF turnover ratio might change if and when options on the ETFs are approved. The comment period for these 19b-4 applications with the SEC ended on Feb 15th, so we may have an answer from the SEC on the matter relatively soon, but no word yet.

Turnover Ratio Higher Than Gold ETFs, But Age May Hold the Key

We also analyzed the overall turnover ratio of bitcoin ETFs compared to gold ETFs. Our findings reveal that bitcoin ETFs exhibit a significantly higher turnover ratio than both GLD and IAU, the top two spot gold ETFs in the US. While the difference in turnover ratios between GLD and IAU could possibly be attributed to options markets, the variance with bitcoin may stem from the relative age of the funds and asset classes. While GLD and IAU are approaching their 20th anniversaries as ETFs, the newly launched bitcoin ETFs have only been in existence for a month. It is plausible that over time, the turnover ratio for bitcoin ETFs may align more closely with that of the gold ETFs. Naturally, even for long term investors to get into the spot bitcoin ETFs at their inception, the overall turnover ratio must be higher at the onset.

Bitcoin ETFs Turnover Converging with the Launch of GLD

When comparing the turnover ratios of GLD and bitcoin ETFs at a similar stage in their lifespan, we notice that bitcoin ETFs initially had a lower turnover ratio than GLD but are gradually converging with GLD. This initial variance could be attributed to the presence of a dominant ETF like GBTC in the bitcoin market, while GLD started with minimal net assets in 2004 and grew steadily through daily fund flows. The fact that the turnover ratios of bitcoin ETFs and GLD are approaching parity just a month and a half after launch lends credibility to our belief that bitcoin ETF turnover ratios may eventually align with those of gold ETFs. We will need to reassess this assumption after five halvings (20 years).

Market Update

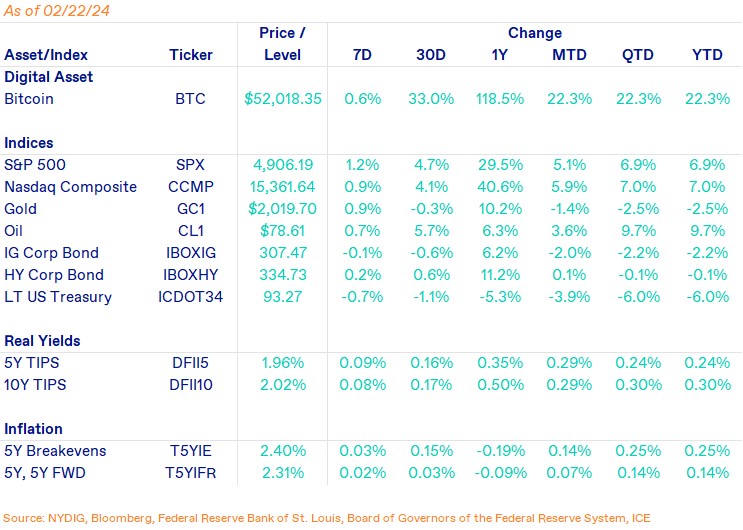

Bitcoin was flat over the week, with little movement intraweek. With the shortened securities trading week due to the holiday on Monday, ETF fund flows were mixed, collecting $351M in aggregate, but with Wednesday showing net outflows for the first time since January 25th. The $51,000 price level appears to be an area of support in the short term, while investors search for the next catalyst, with the halving still 2 months away. Equity markets rallied on the week, with the S&P 500 up 1.2% and Nasdaq Composite up 0.9%. Bonds were mixed as investors continue to grapple with stubborn inflation and forward interest rate expectations. Investment grade corporate bonds were down 0.1%, high yield corporate bonds were up 0.2%, and long term US Treasuries were down 0.7%. Commodities rallied as gold was up 0.9% and oil was up 0.7%.

Important News This Week

Investing:

BTC Order Books Are Most Liquid Since October as Market Depth Nears $540M - CoinDesk

CME Group to Launch Micro Euro-denominated Bitcoin and Ether Futures on March 18 - CME

Regulation, Taxation and Enforcement:

Trump: BTC Has Taken on 'a Life of its Own,' Will Probably Need Some Regulation - CoinDesk

How Su Zhu and Kyle Davies Are Dodging Jail — and Rebranding - NY Mag

Coinbase Letter to the SEC in Response to ETH ETFs - Coinbase

The Real Story of The SEC’s Suit Against Kraken, And Why Kraken Is Moving To Dismiss The Case - Kraken

Companies:

Celsius has Distributed 75% of its BTC Holdings - Court Documents (PDF)

Y Combinator Calls for Stablecoin Startups - Y Combinator

Circle is Discontinuing Support for USDC on the TRON Blockchain - Circle

DCG Calls Out Genesis' Settlement With New York as 'Subversive' - CoinDesk

Social Media Platform Reddit Discloses BTC and ETH Holding in IPO Filing - CoinDesk

Marathon Digital to Start 'Slipstream' to Make Complex Bitcoin Transactions Faster - CoinDesk

Block Says Its Bitcoin Bets, Boosted by the Cash App, Yielded $207M In Gains - Decrypt

Technology:

iMessage With PQ3: The New State of The Art in Quantum-Secure Messaging At Scale - Apple

You Can Now Play Nintendo 64 Games on Bitcoin, Thanks to This Ordinals Project - Decrypt

Early Era Emails Disclosed Between Satoshi and Martti Malmi - GitHub

Early Era Emails Disclosed Between Satoshi and Adam Back - Twitter

Upcoming Events

Mar 12 - Feb CPI reading

Mar 20 - FOMC rate decision

Mar 29 - March CME expiry

April 21 - Bitcoin block reward halving